Senior Editor

Recent events show how aggressively successful fabricators are growing. Last month’s FABTECH® 2011 expo in Chicago broke records with its 500,000 square feet of exhibit space. Capital spending continues skyward after bouncing back from historic lows during the recession. According to the just-released “2012 Capital Spending Report” from FMA Communications Inc., publisher of The FABRICATOR, many fabricators are buying equipment to increase capacity, but more are buying equipment to reduce costs, hinting at just how competitive metal fabrication has become. And most predict capital spending will continue increasing next year.

Meanwhile, a recent study from Deloitte and the Manufacturing Institute estimated that U.S. manufacturing—a sector that has grown much faster than others since 2009—could bring as many as 600,000 people back into the workforce, if only these people had the right skills. As the workforce realigns its skills, unemployment remains high.

For some fabricators, it’s almost the best of times—not roaring as it was in aught-seven, but certainly running at a good clip like 2008. They’re enjoying business from, among other things, the commodities and natural resources arenas, including the shale gas plays that dot the country. (Aaron Brady, global director of IHS CERA, had some positive news in his forecast report for the Metals Service Center Institute. According to his report, “The natural gas ‘shale gale’ shows no signs of stopping.”) For other shops, it remains the worst of times. The recession left some businesses battered, especially those that relied on the construction sector. Meanwhile, all shop owners have been riding a raw material pricing roller coaster.

Many have charged ahead with capital spending over the past few years, and some plan to continue spending into next year. Fabricators also are benefiting from the effects of reshoring, as companies work to shorten their supply chains. According to a Nov. 1 report from the Institute for Supply Management, manufacturing overall slowed in October, but an uptick in new orders was encouraging, as were comments from survey respondents. “Business is very strong, both domestically and internationally,” said one metal fabricator. Another manufacturer serving the transportation sector said what seemed unthinkable two years ago: “Auto industry still is strong.”

Positives and negatives probably will pepper the business climate in 2012. Unemployment will remain high, and businesses will still seek technical talent. Equipment spending probably will continue apace. So will company acquisitions, but they won’t be as prevalent as they could be. Real estate troubles will persist, and governments around the world will continue their struggle to keep their financial houses in order. Mixed together, these ingredients make for a good news-bad news gumbo in 2012 (see Figure 1).

Several years ago many fabricators sent low-ball quotes just trying to get work in the door. This has become less common, according to some, but pricing pressures are still there, driven by technology as well as global and local competition.

The indebted business owner still hangs on, and Ervin Terwilliger has talked with many of them. He is managing partner and co-founder of Elkridge, Md.-based 321 Capital Partners, a financial firm that specializes in distressed-firm transactions in manufacturing, including metal fabrication. Terwilliger explained that many of these distressed firms make enough so they don’t liquidate, but they aren’t being acquired by more successful firms either. Thanks to remaining dysfunctions in the banking sector, in fact, acquisitions haven’t been quite as rampant as they were in past recoveries.

Other observers concur. “I think we’re seeing a bit of a suspended animation when it comes to the economy,” said Chris Kuehl, economic analyst for the Fabricators & Manufacturers Association and managing director at Armada Corporate Intelligence, Lawrence, Kan. “Normally, you let the market do what the market does. It clears things up, and eventually speculators come in and buy up distressed businesses and properties, hang on to them, and they turn it. But now we have a half-in, half-out behavior when it comes to government intervention and even in the private sector. People are not letting things die. There is always a plan around the corner to rescue the homeowner, to rescue banks from toxic debt. We’ve been talking about this since 2009.”

The credit managers are noticing the lackluster credit market, said Kuehl, who also is the economist for the National Association of Credit Management. “There’s just not as much credit activity as one would expect. For instance, the FMA reports are saying that many companies are looking to ramp up capital expenditures. That should be showing in new credit applications and more credit applications being granted.”

There have been some for most of this year, but not as many as expected. This, Kuehl said, started to change significantly in September and October. The number of credit applications is starting to rise.

He added that downward pricing pressures continue unabated, and it’s one reason that the country is not experiencing rampant inflation. Competition— both local and global—is contributing to those pricing pressures, as are new technologies. “We should have by now seen some pretty serious inflation,” he explained. “There’s enough money in the economy. There are hikes in commodity prices, and there is enough demand. Ben Bernanke is probably looking at the situation and saying, ‘Thank goodness!’”

If those downward pricing pressures weren’t there, Kuehl said, the country may well be looking at core inflation in the 3 percent range, which means the Fed would have no choice but to raise interest rates—not what you want for an economy stuck in neutral.

Terwilliger’s firm specializes in transactions involving precision sheet metal and structural fabricators, most with fewer than 50 employees. Distressed-firm acquisition activity has been brisk, he said, “but not necessarily more active than it would be in a better economy. Historically, the factor that drives the distressed transaction is pressure from a creditor.” That pressure isn’t present now, because the banks still have problems of their own, and most are rooted in the economy’s seemingly unshakable albatross: the real estate debacle. Credit Suisse estimates that up to 7.5 million homes are either owned outright by lenders, or have loan payments that are more than 30 days delinquent.

Until the banking system improves, Terwilliger said, “they’re not going to force transactions to happen that would eventually create consolidation, clean up the market, and create liquidity.”

He added that this won’t go on forever, and this year conditions are changing. “We’re seeing some improvement in that fewer players are out there now,” he said. “We see equipment auction values increasing. We’re seeing banks a little more open to taking a loss to save a business and consummate a transaction.”

Terwilliger also sees some unusual opportunities for distressed firms. Banks are considering deals that minimize their losses, deals that wouldn’t have passed muster before the housing bubble burst. “If [the banks] don’t have to take a big loss upfront, they’ll love you, and they’ll do more.”

In these instances, banks have lost the upper hand mainly because of the housing market, he explained. In the past, if a small-business owner couldn’t pay back a loan, the bank would take the loan’s personal guarantee, often the business owner’s house. “In 2004 your house was worth something,” Terwilliger said. “Now the personal guarantee, which used to be the 800-pound gorilla, doesn’t mean so much. Now that owner can say, ‘Listen, I know you’re not going to take my house, because you’ll have a bill if you do. If you take my equipment, you’re still underwater. So let me see if I can maximize return to the bank by structuring a payout to you over time.’”

Kuehl pointed out another trend credit managers are observing: the rise of trade credit. “The machine-tool makers are loaning. They want to sell their machines, and so they are giving people credit to do it. We’re seeing business working with business, and they indirectly engage the banks.”

Other large businesses are doing this too, and often it’s because they have the cash. “Part of the reason [companies hoarded cash] was they weren’t sure what banks were going to do, and they were trying to be frugal.” Now they still have that cash—and they’re using it. “If a customer comes to them and wants to buy inventory, but that customer doesn’t have the money, we’ve got companies now with the ability to float loans,” Kuehl said.

The banking arena notwithstanding, many fabricators predict growth heading into next year—and judging by recent survey data, the industry has some healthy balance sheets to help initiate that growth.

In FMA’s “2011 Financial Ratios & Operational Benchmarking Survey,” 44 percent of respondents said sales have grown by more than 20 percent over the past year, while 18 percent said sales remained steady or fell. Some 12 percent of firms reported operating profits of 20 percent or more, while 8 percent reported operating losses.

A few fabricators reported some eye-opening inventory turnovers. More than half reported fewer than 10 inventory turns a year, but 12 percent reported more than 15 turns a year. A few even reported more than 25 inventory turns annually. Meanwhile, liquidity among survey respondents remains strong, with 60 percent reporting a current ratio of more than 2.0, meaning they have far more assets than liabilities. And assets aren’t all tied up in inventories either; more than half of survey respondents reported a quick ratio of 1.5 or more.

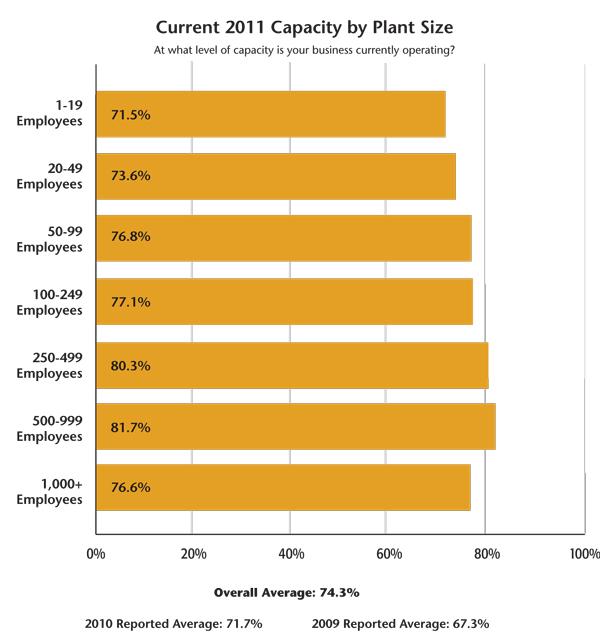

Most metal fabrication in this country occurs in small to midsized enterprises. It’s not surprising that these private companies willing to share their books, even anonymously, often have good stories to tell. But data from this and other surveys, as well as mounting anecdotal evidence, suggests these success stories are becoming more common (see Figure 2).

Consider CAID Industries of Tucson, Ariz., a 235-employee fabricator with a diverse offering, from precision sheet metal fabrication to heavy equipment, tanks, and architectural work. “We had two years—2009 and 2010—when business was off about 25 percent, but this year we’re going gangbusters,” said William Assenmacher, president and CEO. “Our volume is up about 50 percent from last year, or 15 percent from our best year ever. This doesn’t happen too often; you don’t normally come out of a recession and set all your records. We feel very fortunate that we’re in a niche market.”

That niche doesn’t involve just piece-part fabrication, but also entire projects designed and built to order by CAID. Such projects often involve equipment, designed for mining and other sectors, that also requires maintenance and spare parts. This has helped the company gain work at multiple points throughout a product’s life cycle, from development and fabrication to maintenance and repair.

Next year Assenmacher said he expects some copper mines in the U.S. and Mexico to bring in significant revenue. An order for about 25 stainless steel processing tanks also is in the works for Intel microchip plants. “We have a significant backlog for that too,” Assenmacher said. “We’re in the middle of about $3.5 million worth of work for Intel.

“That [kind of work] doesn’t happen very often,” he added. “We’ve been fortunate that when mine work hasn’t been dominating, other work has come in, such as the Intel job, as well as wastewater treatment.”

The company’s capital spending—in new equipment and facility expansion—has remained strong, even through the recession, with annual budgets of $1 million or more, Assenmacher said. “We’re in the middle of a $2 million building expansion right now. That expansion will triple our tank [fabrication] capacity.” The new facility, he said, will not only increase capacity but also decrease competition, because the new building’s higher bays and crane capacities will open the door (literally) for work that few other area fabricators can tackle.

Tom Verboncouer has been noticing his customers invest more in product development. This in turn has brought in more work for Verboncouer’s employer, Robinson Metal, a $50 million fabricator in De Pere, Wis. The contract manufacturer—which serves the food processing, oil and gas, water technology, and specialty machine markets, among others—benefited from 15 percent sales growth this year.

“We’ve added customers because, during the downturn, so many laid people off. We did not, so we had the surplus of talent, and that attracted customers to us,” said Verboncouer, Robinson’s sales and marketing director. He added that customers are demanding more when it comes to quality and delivery. “Price is somewhat of an issue. But we shine when quality and delivery are the main characters of the play.”

For 2012, Verboncouer said he believes business will continue to grow between 5 and 10 percent. “We’ve invested millions of dollars in machinery during the past five years to be ready to do more types of custom work. We’re just sticking with the fundamentals: We have to replace our equipment every so often. If we can do it, we do it.”

Verboncouer also has noticed investors forming holding companies to buy manufacturers of specialty equipment. “They’re giving them the capital to grow,” he said. “These kinds of companies are consistent and connected to consumables: food and other things that just won’t go away. This is kind of the Warren Buffett way.” Buffett has invested in companies like Marmon Group, which has several metal fabrication divisions, and cutting tool manufacturer ISCAR. These companies don’t make many headlines, but over the decades they provide steady returns.

Verboncouer said the packaging industry is going particularly well. As just one example, he described the plastic cups that hold ketchup at fast-food restaurants. Diners can peel the top off to dip fries, or tear and squeeze it to spread ketchup on a sandwich. These new, seemingly mundane products require machines to make them—and those machines use plenty of sheet metal.

“There are traditional things that we take for granted that can be improved upon,” he said. “I’m noticing that these machinery manufacturers have what they call a ‘chief innovation officer.’ This is a creative guy that does nothing but try to innovate. And this person usually works with the chief operations officer. So we have creative people and manufacturing people working together.”

Many expect 2012 to be a lot like 2011. Some companies will grow at a steady clip, but the lingering problems in banking and real estate may prevent overall GDP growth from shifting into high gear. Such economic gumbo may be hard to swallow for politicians, who wish economic cycles followed political ones. But the gumbo tastes sweet for many successful fabricators who, like other manufacturers, have led this country’s drawn-out economic recovery.

Myriad factors contribute to an economy’s success and failure. But at the fabricator level, the situation may not be that complex. Steve Doll, president of Laser Masters Inc. in Houston, boiled down his firm’s growth to two factors: diversification and delivery.

The 28-employee fabricator is enjoying the end of a record year. “I followed whatever the customers were doing,” Doll said. During the past three years the company has almost doubled in size. Not too long ago the shop had only flat-sheet cutting capability. As orders for formed parts came in the door, Laser Masters added press brakes. Next came welding. More equipment allowed the shop to take on more work from various customers from many markets. And thanks to that market diversification, the company wasn’t badly bruised by the recession and continued investing in equipment.

Being successful in metal fabrication, regardless of the economy, isn’t rocket science, he said. “It really just boils down to one thing: Do what you say. If you say you can take the job and deliver it in two weeks, deliver it in two weeks. It is the simplest thing.”

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

In this episode of The Fabricator Podcast, Caleb Chamberlain, co-founder and CEO of OSH Cut, discusses his company’s...

{kind=link}

{kind=link}