Senior Editor

While speaking at The FABRICATOR’s Leadership Summit in Tampa, Fla., earlier this year, Don McNeeley, president and CEO of Chicago Tube & Iron, Romeoville, Ill., said that many fabricators may see business pick up significantly for the second half of the year.

During the ensuing months, after a softening in spring, fabricators saw orders increasing with demand in domestic oil and gas production, solar in the Southwest, and automotive and heavy equipment in the Midwest and Southeast. All this rode the tailwinds of a noticeable reshoring trend. For stateside manufacturing, the future looked somewhat stable, if not bright. In a post-Great Recession world, that was a welcome relief.

Then politics happened.

“It’s been extremely difficult for us to plan,” said Rob Clark, president of contract fabricator Clark Metal Products in Blairsville, Pa., outside Pittsburgh. “It could be a banner year for us, but just as easily, it could be a lousy year for us. When we make calls to customers and start asking them about their forecast for 2014, things are up in the air. We’re heavy into medical equipment, electronics, laboratory testing equipment, and the uncertainty seems to be across the board.”

“2014 is like a visual question mark. We started out 2013 with our best first quarter ever, but our third quarter and fourth quarter are shaping up to be the worst quarters we’ve had in a long time,” said Steve Hasty, president of A&E Custom Manufacturing, a metal fabricator in Kansas City, Kan.

He added that one project has been pushed back thanks to spending cuts from the sequestration. “There are other projects that we were supposed to be able to quote on back in April, May, and June; we are now just getting the [requests for] quotes for those. It seems like everybody is putting their hands in their pockets for a while, and that has been slowing things down.”

“We almost got to the point where the economy was behaving predictably,” said Chris Kuehl, managing director of Armada Corporate Intelligence, Lawrence, Kan., and economic analyst for the Fabricators & Manufacturers Association International®. “Now we’re back to where we were last year when we were dealing with the fiscal cliff. People know that Congress wouldn’t be so stupid as to put the entire country out of business—but they don’t know for sure.”

The October crisis in Washington, including the shutdown but especially the fight over the debt ceiling, has put some business owners into a holding pattern. Why expand, hire, or make deals when the federal government’s dysfunction may again step to the fore in January and February?

“We had a recent conversation with a fabricator that was looking to go to market [to sell the business] in January,” said Christopher Geier, partner in charge at Chicago-based Sikich Investment Banking. “Now they’re waiting to see what happens in January and February before going to market.”

Much of this is anecdotal. Several market indexes released late this year tell a different story. Unexpectedly, the Purchasing Managers Index (PMI™) for manufacturing from the Institute for Supply Management™ trended upward in October—to 56.7—though among the companies that grew, the fabricated metal products sector reported the least amount of growth.

Still, other studies may reveal better times ahead. Kuehl, also the economic adviser for the National Association of Credit Management, produces that organization’s Credit Managers’ Index, which is modeled on the PMI. But unlike that index, the CMI may be a better harbinger.

“The credit decisions occur very early in a business process,” Kuehl said in an October newsletter, “and thus signals future intent. As far as the manufacturing community is concerned, it would appear that the political impasse was of little consequence, at least for the time being. The overall [CMI] moved up from 56 to 57.3, and that is the highest rating since the start of the recession.”

Geier pointed out that when it comes to financing for fabricators, banks continue to be ready to lend—a stark contrast to the lending environment after the financial crisis. “We haven’t seen any negative movement around commercial financing in transactions for fabricators. And this is across industries. Banks are still lending into good transactions and working with good companies.”

According to the Forming & Fabricating Job Shop Consumption Report for the third quarter, published by FMA, overall business outlook remains mostly stable or positive. Only 14 percent of respondents said they had a negative outlook for the fourth quarter (though most of this data came from a survey sent just prior to the government shutdown).

There have been some soft spots, most notably in the mining sector, but many key markets for metal fabricators have rosy outlooks. Edmunds.com predicts domestic auto sales will top 16.4 million in 2014. That’s the largest number the industry has seen since 2007.

Energy sectors are looking good too. In October Deutsche Bank said it predicted 50 percent growth in the global solar business, in which the U.S. has become a major player, particularly with some of the massive installations in the Southwest. And thanks to what’s being dubbed as the “shale revolution,” the U.S. is set to become the world’s largest non-OPEC oil producer, according to an October report from the International Energy Agency. (Though as Kuehl pointed out, complexities abound in the oil sector: Supply may outweigh demand; there’s only so much refining capacity; and, thanks to a law passed after the energy crises in the 1970s, domestic producers can’t export crude oil.)

Meanwhile, according to the 2014 Capital Spending Forecast, released in November by FMA at the FABTECH® show in Chicago, spending projections are surpassing numbers seen even prior to the recession, with projected equipment spending industrywide estimated to be $2.23 billion, a number calculated based on a statistical sample of more than 1,000 respondents. Of course, when it comes to spending projections, timing matters. Data for this survey is from August, before the fall’s political showdown and the uncertainty it created.

Still, the survey shows significant optimism. Companies reporting the highest spending projections were the usual suspects. Automotive parts manufacturers; machinery manufacturers, including agriculture and construction equipment; and commercial HVAC/air-heating equipment topped the list, followed by contract metal fabrication, which includes the largest contract manufacturing operations as well as the smallest job shops. All this supports the reports that activity in automotive and construction could continue climbing into 2014.

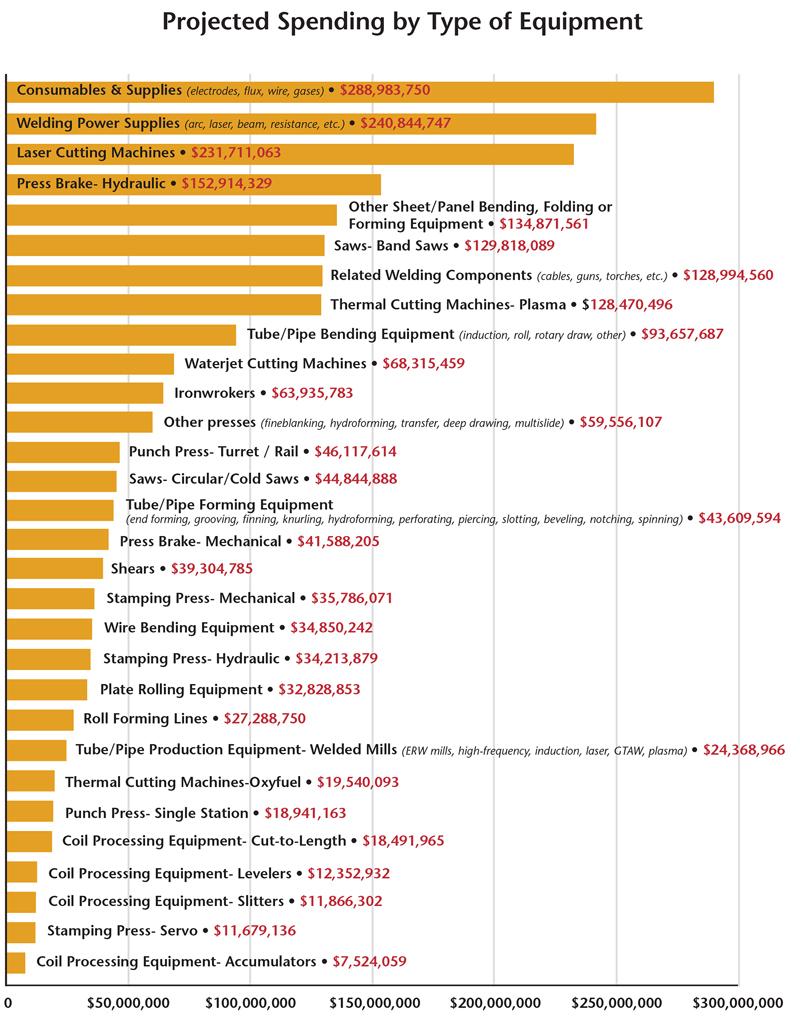

Meanwhile, spending in key product categories is on the rise (see Figure 1). Fabricators expect to spend more than $231 million on laser cutting machines, up 3 percent from last year. Spending increases are even more pronounced for forming equipment. Fabricators plan to spend more than $152 million on hydraulic press brakes, a 6 percent increase from the previous year. And they plan to spend more than $134 million on other types of forming equipment, including panel bending and folding machines. Taken altogether, companies are planning to spend $286 million on forming equipment, more than they plan to spend on lasers and punch presses combined.

From a part flow standpoint, this makes sense. Some of today’s superfast fiber and disk lasers, coupled with material handling automation, can feed parts downstream at an unprecedented rate. Many fabricators have plenty of capacity in the cutting area. Although it varies depending on the part mix, the bottlenecks usually arise in areas that have longer cycle times—most notably bending and, not least, welding—another huge equipment spending area. Fabricators plan to spend more than $240 million on welding power supplies and $288 million on consumables.

All this sounds perfectly healthy. Capital equipment projections for some machines, like plasma cutting and waterjet, aren’t quite up to the levels seen over the past few years, but they aren’t anemic either.

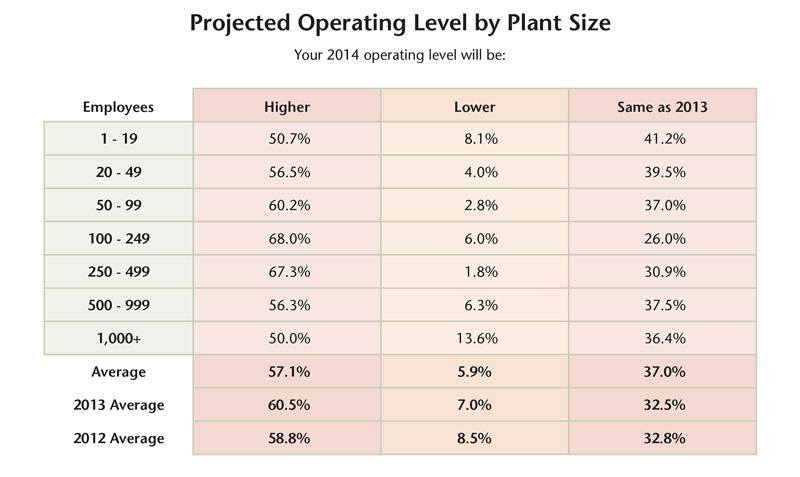

Projected operating levels aren’t anemic either. About 57 percent of respondents projected that their plants would be operating at higher levels next year (see Figure 2). Compared to the previous annual survey, more respondents (37 percent) stated that operating levels would be the same. This makes sense, as fabricators that survived the recession have rebounded and begun to stabilize, returning to slower and (ideally) steady growth.

These survey results fit in with broader projections. According to Kuehl, GDP growth projections for next year range from 2.8 to 3.4 percent. “That gets us a little closer to what used to be our norm. The last few years we’ve been at [a low GDP growth rate that] doesn’t fix any problems. We need to be at 3.5 percent GDP growth to feel healthy.”

At the same time, in September the Fed projected the unemployment rate in 2014 to decrease to as low as 6.4 percent (though that number doesn’t count the people who have stopped looking for work).

And unlike before the financial crisis, new jobs—not debt— are driving consumer spending. As Dan Meckstroth, chief economist for the Manufacturers Alliance for Productivity and Innovation (MAPI), stated during a presentation in September, “Consumption is being driven by new jobs, people earning new incomes. A relatively small amount of consumption is being driven by wage increases of currently employed people. So we’re really dependent on job growth to keep consumer spending going.”

Here again is where uncertainty arises. Manufacturing overall has lost 2.3 million jobs and regained only 500,000. However, according to an analysis from McKinsey & Co., a consultancy, the fabricated metal products sector—which includes thousands of small contract manufacturers and job shops that send parts up the supply chains to larger OEMs—has collectively contributed more to job growth than any other manufacturing sector.

Even so, that adds up to only 179,000 jobs, a drop in the bucket of overall job growth since the recession. As Meckstroth said during his talk, most of the job growth has come from the service sector, like retail and food services, as well as health care. This includes jobs requiring either a high skill level or very little skill, and there are few jobs in between.

Will these jobs be enough to sustain long-term economic growth? That concerns many, but even this hasn’t been enough to hamper growth in much of manufacturing. According to some owners in metal fabrication, however, the government’s fiasco in October changed things. Perhaps this new level of uncertainty was the straw that broke the back of business forecasting.

At the same time, though, economic fundamentals remain relatively sound, and forecasts for various sectors fabricators serve aren’t dire. One thing is for sure: Most can’t wait to get the government’s budget battle behind them.

No matter what the economy does in 2014 and beyond, no one can escape demographics. Visit a shop owner in this business, and you’ll probably see a few gray hairs.

Lane Moyer, a corporate lawyer with Chicago-based Vedder Price, works with various companies, including many in the metal fabrication space. He sees a landscape dominated by extremely small firms. In the past, many of those firms were passed on to the next generation. But compared to the retiring baby boomers, the next generation just isn’t as populous, so many shop owners will be looking for buyers.

He added that the successful firms will grow organically or by acquiring other small firms. Once the company grows large enough—say, more than $10 million in sales—it will start looking for buyers, be they strategic (competitors or firms with complementary offerings) or financial, be they private equity players or long-term investors. Regardless, one way or another, the business may well see some consolidation, and big players may continue to get bigger.

“You can just see it coming,” said Moyer, who also sits on FMA’s Business Valuation Committee. “I get more calls from people who say they’re not ready to sell, but they’re looking down the pike three to five years, and they hope to sell their business. We’re seeing a demographic shift. What will drive these transactions is the owner’s desire to retire.”

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

In this episode of The Fabricator Podcast, Caleb Chamberlain, co-founder and CEO of OSH Cut, discusses his company’s...

{kind=link}

{kind=link}