Contributing Writer

Figure 1: When looking at this sample part, you notice that the estimator makes it clear that the part requires hole-making, bending, deburring, finishing, and part marking.

This edition of Precision Matters continues our detailed examination of estimating as a business process. The previous edition covered the need to identify the required manufacturing steps and to verify that those steps are in line with the shop’s business mission.

As those needed manufacturing steps are logged in the estimator’s notes, they represent expenses that must be included in the estimate (see Figure 1). In some cases, those notes closely resemble a hypothetical “work order” or “traveler” used to coordinate the flow of work through the manufacturing department.

For the sake of discussion, we’ve dissected the estimator’s job into a dozen topics. In reality, these topics may overlap or evolve in different sequences. As a review, here is a brief outline of how we’ve dissected an estimator’s job:

To illustrate how similar estimating might be to job costing, consider a project that is accepted on a “time and material” basis. The customer agrees to pay whatever it costs, plus a profit to the shop. All the estimator needs to do is add up the expenses for material, machine hours, machine labor, and the shop’s consumables used to complete the job. The sales team then adds whatever margin is needed. All we need is a report on what the job cost.

It’s the estimator’s moment of bliss: certainty of time and material expended to complete the job. The completed work order shows the exact sequence of manufacturing steps that were needed. The actual start and stop times for each operation are shown. The raw material condition before and after each step is recorded. Yield for each operation is no mystery. Each operation even has a detailed narrative, shown on our imaginary work order, that explains the tooling selection, special handling, or subcontracted actions. The amount of detail varies from project to project. However, the estimator does not need to write any of it for this project because the production manager completed all of that detail. The labor of costing a completed work order is very straightforward when compared to the effort of predicting these manufacturing expenses beforehand.

Job costing is a necessary function. The reports are useful aids in identifying deviations from normal. When things don’t go as expected, the business is harmed. Obviously, if the job costing reports show that a particular type of work is expensive, a company might focus on ways to reduce its costs through better equipment or better training. On the flip side of that coin are job costing reports that reveal efficient behavior.

Job costing is similar to estimating in that expenses are totaled for each manufacturing operation. The main categories of expenses are labor, machinery, material, and overhead.

Unlike job costing, estimating lacks certainty. Fortunately, the inability to be exact does not prohibit one from the act of predicting. Predictions are just better educated guesses. We can improve the accuracy of our estimates by minimizing the number of bad guesses. Well, duh!

For example, we can study the machine’s documentation to determine its cycle speed. We then can guess that our machine operates as the manual claims. Alternatively, we can gather historical data on the throughput of the machine. We can watch and time the activities in the workcell and determine what values to use when estimating a cycle rate for our workcell, and perhaps even establish a normal setup time.

While an estimator’s log of predicted expenses (see Figure 2) and a production manager’s work order (see Figure 3) serve different purposes and satisfy different priorities, they should not be strangers to one another. It is bad to have the estimator imagining expenses that are irrelevant when it comes to actually manufacturing the product.

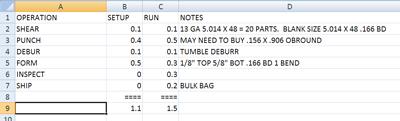

Figure 2: An estimate is not going to have all of the details that will be found in a work order.

How could such craziness happen? The estimate might have been based on using a machine that is temporarily out of service. Instead of CNC machining, this batch was produced with manually operated machines. Yes, the cost for this batch was higher, but the customer’s expectation for delivery and functionality was satisfied. This type of event is not too alarming.

However, if the estimate was based on using dedicated tooling to save time and setup, while the work order never took that tooling into account—perhaps the first piece was prototyped without the tooling—it is likely that the setup times and schedules for the product are consistently out of line with the estimate. Yep, this is another call for internal feedback and review of estimates and completed work orders. Estimators and production managers are nearly as inseparable as estimators and sales managers.

As a business process, the translation of an estimate into a work order should be seamless and well-coordinated. Estimating should be aware of the need for accuracy and detail on the work order—the exact sequence, the exact material, and the right schedule. Manufacturing should be aware that the estimate is prepared in a “maybe” context. There is no certainty that the estimator’s effort will translate into a production order. The estimator/sales effort is focused on timely and responsive customer service. Accordingly, some details must be generalized simply for the sake of speed.

One of my favorite shortcuts when estimating is to skip writing the narrative for each manufacturing operation. As shown in the example in Figure 3, a work order for a sheet metal part might start with “SHEAR (6) STRIPS 5.014 x 48 – (20) ON.” The equivalent estimate might be not much more than “Shear” with a few reminders about blank size and expected yield. Compare Figures 2 and 3 to see how the estimator’s view differs from the production manager’s view. And they’re both looking at the same part shown in Figure 1.

True! The estimate predicts the work order, so the two should match. That’s just common sense. The less the two match, the more internal pressure on the business emerges, usually in the form of squawking about costs.

Common sense is a funny thing. For example, in the actual production work order, the parts might be nested to better utilize the raw material. The estimate is likely to be based on the cost for material without optimized nesting. You want the production manager to have maximum flexibility to maximize the operating margins. Discretionary nesting is a blessing. (There’s a topic you can discuss with your spouse.) The estimator, however, cannot always count on the parts being nested efficiently.

As a point of conversation, let’s suppose that 80 percent of the time, the manufacturing operation goes perfectly with no scrap. That also could be described as 100 percent yield for the operation. For those occasions, the job costing version of an estimate is OK. What does the estimator do about the 20 percent of the time when things don’t go right?

If the priority is speedy delivery of a bid, then the estimator might resort to guessing about how much extra raw material to feed the operation to guarantee enough material for the next operation.

Over time, each workcell’s performance in terms of yield becomes apparent. The estimator’s toolkit will include standard cycle times and setup times, as well as yield rates for each operation.

Going back to the estimator’s bliss of costing a completed work order, the start and stop times for each completed operation made it convenient for calculating machine expense for each operation. Those of you with fabricating experience might object to my claim of convenience. Setup times matter greatly to the estimator and might be useful to the scheduler, but the production crew doesn’t care about setup time versus run time discussions. It often is challenging to distinguish when setup ended and run time began—or resumed, in some cases. Production people should focus on production, not necessarily on precision time-logging. Not only that, but machine hours and employee hours are not always recorded clearly on the work order or traveler. For instance, a workcell might have one person loading a CNC machine every five minutes for 20 seconds. The rest of the time the employee uses a drill press to remove burrs from the parts. The labor hours were not entirely spent on either the CNC mill or the drill press. The CNC mill ran unattended for a significant portion of the time. And what about quality control? Do we put a stopwatch on the inspectors?

Figure 4: Calling up a program before initiating a job in a machining center is an example of one setup activity.

False! Work orders and estimates are seldom the same. The estimate is merely a log of predicted expenses. Specific sequence does not matter so much as avoiding omissions. The work order directs and records labor. It is specific and time-dependent.

OK, it is bad when the author argues with himself and loses. Indeed, an estimator’s outline of needed manufacturing steps is different from a detailed production work order. Job costing and estimating are not the same. I admit it. For the purposes of preparing a rapid price estimate for delivering a specific quantity with a given lead-time, the distinction between labor hours and machine hours might be needless detail to the estimator. Writing out a full narrative for each operation might be a waste of the estimator’s effort—this is an evaluation you’ll make on a case-by-case basis.

As an event in the estimating process, we need to predict the amount of time it will take to complete a manufacturing operation. We have to consider three kinds of operations: subcontracting, indirect labor, and direct fabrication.

For subcontracted operations, the prediction of direct expense often is a matter of obtaining a price quote from the subcontractor. The prediction of time serves primarily for estimating the lead-time for the project. While labor might be expended in transporting the project to and from the subcontractor, it is reasonable to handle it as indirect labor.

Indirect labor represents expenses that exist regardless of what is being built. Examples of indirect labor are sweeping the floor, driving the forklift, or receiving raw material. This overhead expense is a constant, frequently expressed in an hourly rate. The accounting department provides the rate to the estimator. Accounting uses historical data to estimate the direct and indirect operational expenses for the firm. The estimator may need to deal with estimating the staging time between operations—again for estimating the lead-time. However, the indirect expenses frequently are built into the hourly rates for each in-house operation.

Direct labor represents expenses that are attributed clearly to a specific project. Drilling a hole, bending a flange, painting the part—this is the stuff that estimators are involved in predicting. Here, we need to predict time both for scheduling purposes and for determining expense.

The estimator might view a manufacturing cell in two ways: as something that is in full-speed production and as something that is not. When the cell or operation is in full-speed run mode, it is set up. When it is not set up, it is either being set up, being torn down, or is idle.

Total time for this fabrication step can be determined by T = (Q x R) + S. T is the total time. Q is the quantity of the parts. R is the time per part. S is the setup time.

The estimator makes an effort to distinguish between setup and run time. If you know the setup time for a batch, where regardless of batch size the setup time will be constant, and you know the cycle time for each part, then you can predict how much time any given quantity of parts will take to produce. This information about time per batch is useful to the estimator when establishing a lead-time for the project. Lead-time is the number of days in advance that the customer must place the order to get the parts on a specific date.

For our discussion, setup means all of the time required to prepare the machine for production of a specific project (see Figure 4). The teardown time and the transfer of material to the next queue are considered to be indirect expenses. Your shop might prefer to include setup and teardown in the estimated operation expense time.

Dedicated staff might perform setup, while other employees handle the production run. Regardless of how it is performed, setup will take about the same amount of time, from batch to batch, regardless of how many parts are being built.

Each shop determines what setup includes. Tooling selection, tooling installation, calibration of the operation, safety device setup, testing, first-article inspection, and operator qualification—these are likely to be part of the setup process.

Setup is simply a matter of preparation to do something. The estimator needs to predict that setup time. The prediction may not be exact for every batch of parts, but it is based on historical data. With that setup time estimated, converting it to a dollar amount is simply a matter of multiplying by the shop rate for that operation.

The sales group is responsible for reporting how the setup expense is reported to the customer. Some customers want the setup expense reported as a separate line item. Others prefer to have the setup included in the piece part price. To do that, the estimator simply divides the total setup expense by the total number of parts and then adds that to the other part expenses.

When the operation is in full production, it usually is possible to predict how many parts will be produced per unit of time. The estimator needs to predict the cycle speed of the operation—time per part—for the production mode. Again, this production rate should be fairly constant regardless of the number of parts.

The production expense for a fabrication operation is determined by E = P x T x M. E is the production rate. P is the number of parts. T is the time per part. M is the hourly machine rate.

For each production run, there is an efficiency curve—usually a bell curve—that reflects the learning curve. After a few repetitions, the operator’s speed improves. After boredom sets in, a sag in productivity might be evident. This nuance might be important to some estimates. However, the shop should be able to establish time standards for each operation that the shop offers to its customers. This is the normal time that it takes to set up a machine, as well as what its cycle rate is.

We would be delighted to hear from you to help us improve this discussion of estimating. If you have any observations on this subject matter, please let us know.

Gerald would love to have you send him your comments and questions. You are not alone, and the problems you face often are shared by others. Share the grief, and perhaps we will all share in the joy of finding answers. Please send your questions and comments to dand@thefabricator.com.

Let’s see how a shop might answer an important question about one of its most vital shop floor activities: What is the cost for a forming operation?

The quantity is a batch of 100 parts. The standard setup time for the press brake is 30 minutes per bend. The shop expects it to complete a bend every 12 seconds. The press brake setup time is billed at $80 per hour. The press brake run time is billed at $60 per hour. Please amortize the setup into your piece part price for this forming operation.

Oh, yes. There is only one bend in each part.

Let’s start with the setup cost first. We have only one setup operation for this project, so our total setup time is 30 minutes. To convert 30 minutes into a useful number of hours, divide the number of setup minutes by the number of minutes in an hour. In this instance, we arrive at 0.5 hour.

Finally, to calculate the total setup in terms of money, multiply the number of hours by the price per hour—0.5 hour x $80 = $40. That’s $40 for the setup for a batch of 100 parts.

Now, let’s calculate the expense for the run time. Multiply time per part by the number of parts—12 seconds x 100 parts = 1,200 seconds. Divide the number of seconds by 3,600 to convert to hours—1,200/3,600 = 0.34 hour.

Multiply the number of hours by the price per hour—0.34 hour x $60 = $20. That’s the total expense for run time.

Add the $40 setup to the $20 run time, and you arrive at $60 for the operation. Divide that by the number of parts in the batch—100—to get the per-piece price for this forming operation. I came up with an answer of $0.60 per part.

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

In this episode of The Fabricator Podcast, Caleb Chamberlain, co-founder and CEO of OSH Cut, discusses his company’s...

{kind=link}