President/CEO

Steel pricing is the product of a complex interplay between supply and demand, along with other factors such as ferrous scrap prices and foreign steel import levels. Factor in the unpredictable nature of President Donald Trump’s trade actions, and steel prices have become increasingly difficult to predict.

The Trump administration restricted imports by imposing Section 232 tariffs of 25 percent on steel and 10 percent on aluminum effective June 1. Quota agreements were reached with Argentina, Brazil, and Korea. The goal is to safeguard the nation’s security by ensuring that essential industries such aluminum- and steel-making are not threatened by unfairly traded imports. Less competition from foreign mills and healthy demand from a strong U.S. economy have allowed domestic steelmakers to keep prices unusually high. One steel company after another announced record profits in the second quarter.

Trump threw the market another curve in the early morning hours of Aug. 10 when he doubled the tariffs on Turkey. He declared via Twitter: “I have just authorized a doubling of Tariffs on Steel and Aluminum with respect to Turkey as their currency, the Turkish Lira, slides rapidly downward against our very strong Dollar! Aluminum will now be 20% and Steel 50%. Our relations with Turkey are not good at this time.” The new tariffs became effective Aug. 13.

The Turkish steel industry is a major buyer of ferrous scrap from North America and was the eighth largest exporter of steel products, including rebar, cold-rolled coil, galvanized coil, oil country tubular goods, standard pipe, and hot-rolled coil, to the U.S. over the past year. The 50 percent Section 232 tariff, on top of antidumping and countervailing duties already in place, render Turkish imports uncompetitive and effectively eliminate them from the U.S. market.

It is difficult to gauge the impact of this decision on the U.S. steel market. At least in the short term, it could put downward pressure on ferrous scrap prices, and thus steel prices, assuming Turkey purchases less scrap from the U.S. On the other hand, less competition from Turkish imports of finished steel products stands to support higher prices from domestic mills that move in to fill the gap.

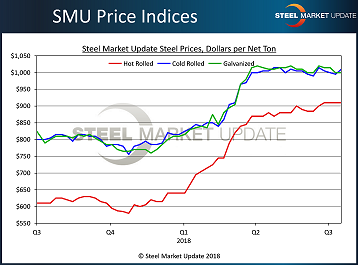

Steel Market Update (SMU) is beginning to see signs that steel prices have peaked and are more likely to decrease than increase in the coming months (see Figure 1). SMU’s surveys indicate that lead times on steel orders are shortening, which suggests the mills are not quite as busy. Buyers tell SMU that the mills are more active and willing to discuss price during negotiations.

One of the major mills, ArcelorMittal USA, announced a $30/ton price increase on cold-rolled and coated products on Aug. 14. This is not necessarily a sign of strength. Rather, the mill is hoping to improve profitability by increasing the currently narrow spread between hot-rolled and cold-rolled/coated products to more normal levels.

Pricing on galvanized steel may be poised for a dip as the coating extra for zinc comes into play. The price of zinc, which is used to give galvanized its corrosion-resistant coating, has declined precipitously in the last few months, from more than $1.60/pound to as low as $1.05/pound in recent trading. If the low price shows some staying power, the mills are likely to adjust their extra charge for zinc.

SMU’s Price Momentum Indicator has been at neutral since July 10, meaning steel prices are in transition and could move in either direction over the next 30 to 60 days. But if not for the Turkey tariff situation still playing out, SMU would have adjusted its Price Momentum Indicator to Lower for flat-rolled in mid-August.

The following were SMU’s benchmark steel prices, FOB the mill east of the Rockies, as of Aug. 15:

Figure 1. Over the past several months, steel prices appear to be retreating from recent highs.

SMU regularly canvasses the market to measure what steel buyers are thinking. The most recent poll in early August showed:

What seems to be concerning steel buyers the most these days is not demand or supply, but the seemingly capricious nature of Trump administration trade policies. As one executive commented, “The Turkish situation will definitely cause some headaches for many and introduces new uncertainty into the market. Anyone looking to import has to ask: Which country might be next?” Said another: “It demonstrates the power vested in one man to impact global markets with the stroke of a pen, or perhaps a tweet.”

SMU conducts various steel training workshops around the country in conjunction with a domestic steel mill. Our first “Steel 201: Introduction to Advanced High Strength & Other New Steels” workshop will be held on Sept. 11-12 in Middletown, Ohio. Attendees will tour the AK Steel Research and Innovation Center as well as the fully integrated Middletown steel mill.

On Dec. 11-12 SMU will conduct another one of our “Steel 101: Introduction to Steel Making & Market Fundamentals” workshops in Toledo, Ohio. Attendees will tour North Star BlueScope’s electric-arc furnace and rolling mills.

Information about any of these workshops can be found at www.steelmarketupdate.com/events.

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

In this episode of The Fabricator Podcast, Caleb Chamberlain, co-founder and CEO of OSH Cut, discusses his company’s...