President/CEO

Where will steel prices be heading in the coming weeks? No one really has any confidence in answering that question.

Are steel prices witnessing a dead-cat bounce or the beginning of a bullish reversal? The market appears split on the feline versus bovine analogy. In other words, a huge divergence of thought exists on what is going to happen to steel prices over the next three or four months.

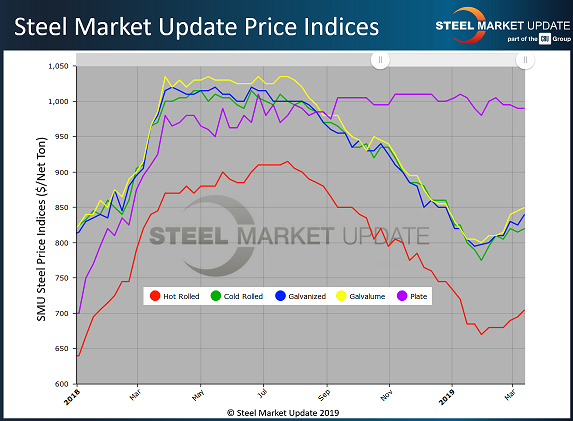

The benchmark price of hot-rolled coiled (HRC) steel peaked at around $915/ton last summer, according to the Steel Market Update HRC Index. HRC then began a steady descent that took it down to $670/ton by late January—a 27 percent decline. Since then the price has recovered, moving to over $700/ton. Will this be a soft bounce, or is it the beginning of a bull run?

Some bullish analysts forecast that the price of hot-rolled steel could run back up as high as $900/ton. With an assist from the Trump administration’s Section 232 national security tariff, which puts a 25 percent duty on foreign steel, domestic steel mills are operating nearly at full capacity. With less competition from imports and pent-up demand from the harsh winter, the mills are hoping to collect two $40/ton price increases announced in January and February, with more likely to follow if those prove successful.

In the dead-cat camp are analysts who are concerned about the staying power of Section 232 tariffs, which are being challenged in Congress, in the courts, and in various trade negotiations. It appears increasingly likely that the Trump administration will have to rescind the tariffs on steel imports from Canada and Mexico to secure passage of the U.S.-Mexico-Canada trade agreement sometime this year. Opening the U.S. border to steel from the north and south could cause a surge in supply and drive prices back down to $600/ton, making the recent uptick in prices just a short-term bounce.

As of March 12, Steel Market Update’s Price Momentum Indicator was set at “higher” on flat-rolled steel, as lead times have begun to extend and prices have begun to move up following the mills’ two announcements (see Figure 1). (All prices are FOB the mill, east of the Rockies.) The price of hot-rolled steel averaged $705/ton ($35.25/cwt), with lead times of three to six weeks. Cold-rolled steel was selling at an average price of $820/ton ($41.00/cwt), with lead times of five to eight weeks. The benchmark price for galvanized 0.060-inch G90 coil averaged $918/ton (45.90/cwt), with a lead time of five to eight weeks. For Galvalume 0.0142-in. AZ50, Grade 80, the average price was $1,141/ton (57.05/cwt), with a lead time of six to nine weeks.

For steel plate, the SMU average was $990/ton ($49.50/cwt) FOB delivered to the customer’s facility. SMU’s Price Momentum Indicator on plate was “neutral,” meaning prices were expected to remain steady over the following 30 to 60 days. This shift occurred because SSAB made a $40 price increase announcement a few days prior to this article being written, and it is SMU’s policy not to influence the market when announcements are made. Plate lead times were six to nine weeks.

Steel Market Update canvasses the flat-rolled and plate steel markets twice a month through the use of a questionnaire to end users, service centers, steel mills, and trading companies. One of the key indicators SMU tracks is whether service centers are raising prices or continuing to offer discounts. The latest survey results show that flat-rolled service centers are beginning to support the concept of higher steel prices. Distributors are raising spot pricing on their end-user customers, which is helping to support the price increases announced by the domestic mills.

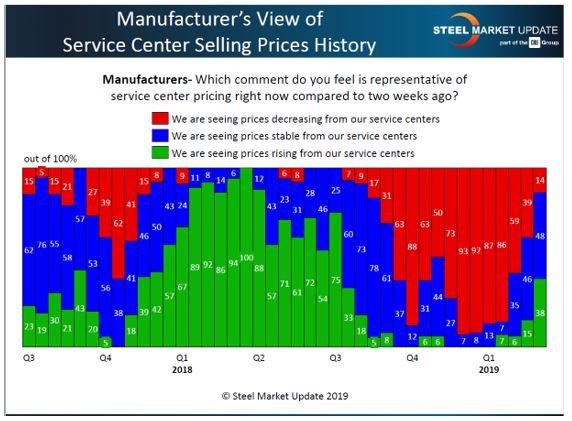

In the first week of March, 38 percent of the manufacturing companies responding to SMU’s questionnaire reported that their service center suppliers were raising spot prices—twice the percentage reported two weeks prior. At the same time, the percentage of manufacturers who reported falling spot prices declined from 39 percent to 14 percent (see Figure 2).

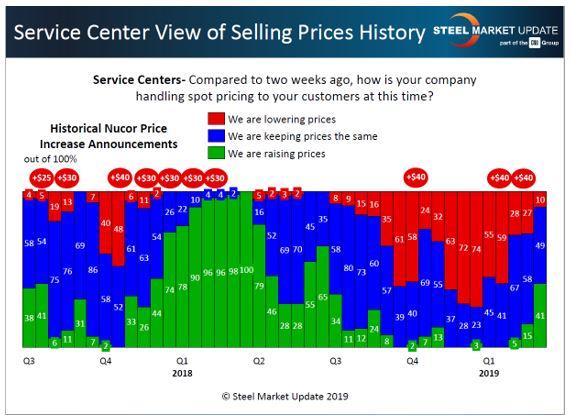

Service centers, responding independently from the manufacturing companies, reported similar results. Forty-one percent said they were increasing pricing to their spot customers. Only 10 percent admitted they continued to offer discounts to customers to secure the sale. Figure 3 shows the service center results.

What does the future hold? There is no clear consensus. Here’s what steel executives polled by SMU are saying about mill lead times and the current pricing environment:

Figure 1. With steel price increases looking like they might not erode anytime soon, will the steel mills feel confident enough to continue the trend, or will changes in the Section 232 tariffs situation end any momentum for further price hikes?

Based on executives’ comments and survey results, Steel Market Update believes spot steel prices will continue to rise gradually over the next 30 to 60 days, at least as long as the tariffs remain in place. If Trump rescinds Section 232 tariffs on some countries or replaces tariffs with quotas, all bets are off on how the market will react.

Registration is open for Steel Market Update’s next Steel 101: Introduction to Steel Making & Market Fundamentals workshop, which will be held in Davenport, Iowa, May 14-15. The workshop will include a tour of the SSAB Montpelier, Iowa, plate mill. For details, visit www.steelmarketupdate.com/events/steel101.

It’s also time to register for Steel Market Update’s Steel Summit Conference, Aug. 26-28, in Atlanta. More than 1,000 industry executives are expected to show up for the educational and networking event. You can find the program, speakers, costs, and registration instructions at www.steelmarketupdate.com/events/steel-summit.

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

In this episode of The Fabricator Podcast, Caleb Chamberlain, co-founder and CEO of OSH Cut, discusses his company’s...

{kind=link}