President/CEO

The decrease in demand for steel is nothing like what steel mills saw in 2009. Getty Images

Steel Market Update (SMU) has been asked: How does the COVID-19 pandemic compare to the Great Recession in terms of its impact on the steel market? The full effect of the coronavirus crisis on the U.S. economy and steel demand is still to play out, of course, but some comparisons can be made. Generally speaking, steel production and steel prices have declined more sharply in the past few months, but to a lesser degree than during the 2008-2009 recession.

SMU surveys steel buyers twice each month to track market sentiment. Buyers’ optimism or pessimism offers some insight into their likely decision-making. SMU’s Buyers Sentiment Index offers a sharp contrast between current attitudes and the way folks were feeling during the Great Recession. As of mid-April, the index had a reading of -4—down dramatically from +58 just the month before—but still considerably more optimistic than the all-time-low reading of -85 hit in March 2009.

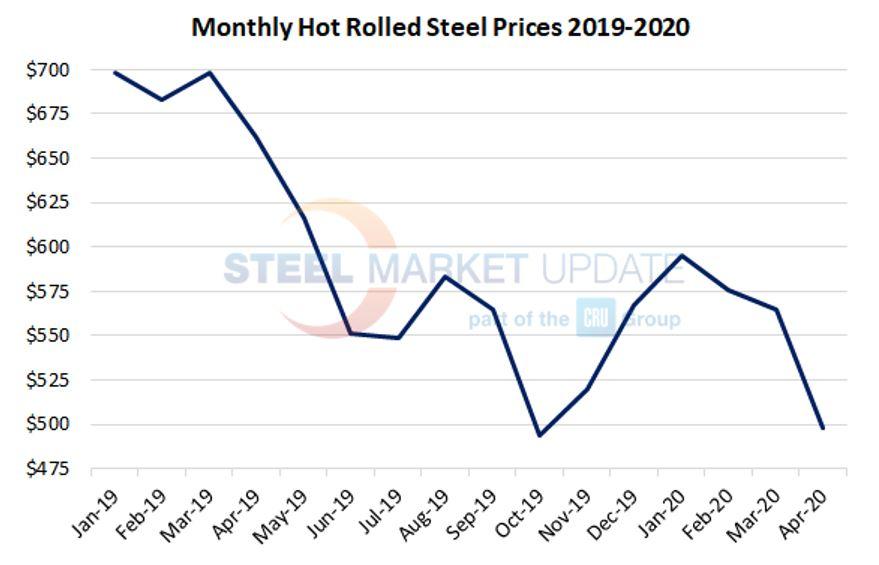

Both economic collapses were severe and unexpected, and both took a serious toll on steel demand and prices. Looking at the mill utilization data from the American Iron and Steel Institute for March and April 2020, capacity utilization declined from more than 80% to around 56% in less than a month. During that period, the benchmark hot-rolled price declined by roughly 15%, from $580/ton to $495/ton (see Figure 1).

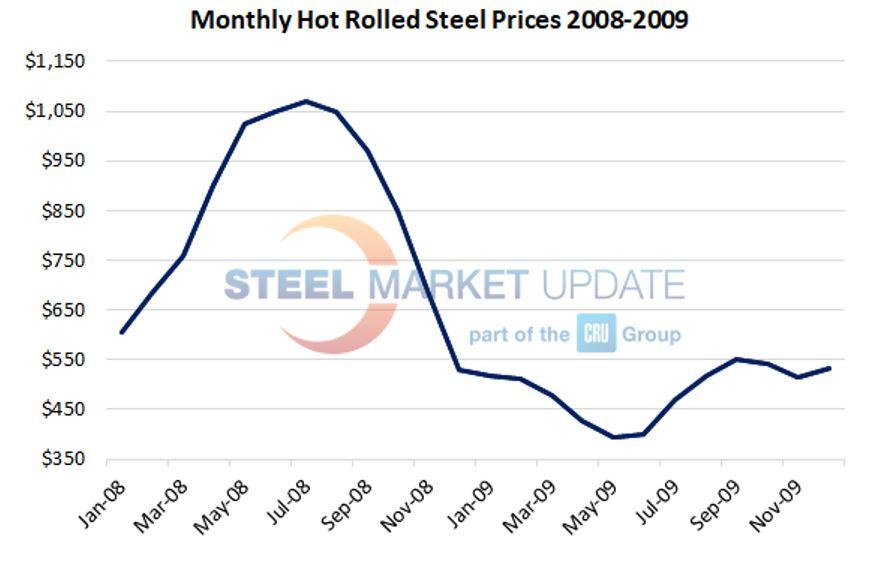

In comparison, in the summer of 2008, U.S. mills were cranking out steel at 90% of their capacity to capitalize on inflated hot-rolled market prices in excess of $1,000/ton. When the real estate bubble burst, sending the economy into a tailspin, the price of steel lost half of its value, to around $500/ton, in a period of about five months. In the same 19-week period, mill capacity utilization plunged from 90% to 33% as the recession slashed steel demand.

Steel prices did not immediately recover once the capacity utilization hit bottom at the end of August 2009. Prices continued to languish for another five months, hitting bottom in early June 2009 at $380/ton (see Figure 2). The subsequent recovery was prolonged and slow due to excessive inventories having been accumulated throughout the supply chain.

Being more proactive this time around, the domestic mills have acted quickly to idle some 10 million tons of their annual capacity in an effort to match supply with the declining demand and put a floor under steel prices.

Whether steel prices continue to decline or level out in the coming weeks or months depends on several factors. Before the government was forced to shut down commerce and enforce social distancing back in March, the economic fundamentals were strong, arguably much stronger than the economy of 12 years ago that was propped up by an inflated housing market. So, recovery from the pandemic could be more V-shaped, according to experts.

Ferrous scrap prices are an indicator of finished steel prices. Unlike in 2008, scrap collection is an issue today as dealers must avoid COVID-19 infection. Less prime scrap is available from auto plants and other manufacturers that have been forced to suspend production. Thus, scrap prices are likely to firm up as supplies tighten.

Service centers have been doing a much better job of managing inventories compared to the Great Recession. SMU proprietary service center inventories data put flat-rolled inventories at 2.5 months’ supply (based on March shipping rates), which would be considered “balanced” in a reasonable market. These inventories will become inflated over the next couple of months, but buyers are making adjustments to accommodate anticipated lower volumes.

Steel demand remains the big question. How much of the business will come back once the virus is behind us, and how much will be lost for good? Negative forecasts for automotive sales and oil prices don’t bode well for steel in the near term, but sources tell SMU that activity is still fairly strong in some sectors of the economy, such as construction and agriculture, and in some regions of the country.

Figure 1. The coronavirus crisis has resulted in a sharp decline in steel demand, and prices have dropped as a result.

Distributors have put purchasing on hold, but will be quick to come off the sidelines at the first signs of a turnaround. Steel could get tight if the recovery of demand outpaces the mills’ ability to restart production. It will be critical for steel buyers to keep a close eye on the market to make sure their company does not get caught short. This year steel purchasing agents will be juggling supply and demand as never before. Everything is one big question mark.

Comments from service center and manufacturing executives responding to SMU’s April 13 survey reflect the weight of their worry over the coronavirus crisis:

Steel Market Update is hosting a free weekly Steel Community Chat every Wednesday at 11 a.m. ET. The webinar includes guests such as analysts, economists, and industry executives. The webinar is at no cost and open to all. You do not have to be an SMU subscriber. You can register for the next event here.

Our Steel 101: Introduction to Steel Making & Market Fundamentals Workshops have been postponed pending the reopening of business and when companies feel comfortable allowing employees to travel. We do not anticipate an “in-person” Steel 101 until September, when we are scheduled to conduct a workshop in Hamilton, Ont., Canada, and tour the ArcelorMittal Dofasco fully integrated steel mill.

SMU conducts the largest flat-rolled and plate steel conference in North America. The SMU Steel Summit Conference is still scheduled for Aug. 24-26 in Atlanta. We are carefully monitoring government instructions and the medical community to see if an end-of-August conference will be safe for attendees. We anticipate making a final decision as to whether the conference will be canceled in mid to late May.

SMU also is looking at taking its training workshops and conference “virtual,” if it makes sense. We will have more information about our online plans soon.

Figure 2. To give current steel buyers some perspective about today’s hot-rolled steel pricing trends, notice the heights from which steel prices fell toward the end of 2008. Prices cratered at just below $400/ton in the early summer of 2009.

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

In this episode of The Fabricator Podcast, Caleb Chamberlain, co-founder and CEO of OSH Cut, discusses his company’s...