Senior Editor

Steel mills announced price hikes roughly a month ago, but declining demand hasn’t done much to support that effort. Niteenrk/iStock/Getty Images Plus

Has the U.S. steel market reached another downward inflection point?

I asked in my last column whether the market was turning upward or whether it was just a “dead cat bounce.” Hindsight is 20/20. And it looks like we’ve got a dead cat.

Case in point: Our survey data has turned a little bearish following an upsurge in sentiment that, in retrospect, might have crested not long after SMU’s Steel Summit conference.

It wouldn’t be the first time we saw post-conference euphoria in August fizzle out in September. Last year, the talk of Steel Summit was whether hot-rolled coil (HRC) would hit $2,000/ton. Prices peaked at $1,955/ton in September and then fell through the end of the year and into early 2022.

You’ll recall that several mills announced price hikes immediately after the close of Steel Summit this year, perhaps just as some of you were boarding your flights home. Did the August increases, $50/ton to $75/ton depending on the mill, stick?With a month of survey data behind us now, the consensus is that they stuck in part, or perhaps not at all (see Figure 1). Very few mills achieved their stated objective with the price hikes.

Those survey results roughly match trends in our pricing data. Our HRC price was at $800/ton in mid-August, and it’s since stagnated just below that level—up a little one week, down a little the next, but not managing to cross that $800/ton threshold since.

Don’t get me wrong. That’s way better than the $50+/ton per week declines we saw earlier this year. That’s when prices were in freefall after the initial shock of the war in Ukraine passed. But, as far as price increases go, that last round in August looks like it didn’t do much more than stop the bleeding.

Could mills announce another round of price hikes to shore up the first? That’s a tried-and-true play. But it’s harder to pull off in the immediate aftermath of scrap prices falling in September. It’s also hard to do when most buyers tell us that producers are willing to negotiate lower prices for sheet and plate (see Figure 2).

Some market participants warn of the possibility of a strike or lockout at U.S. Steel given that the Pittsburgh-based steelmaker and the United Steelworkers (USW) union are now well past the Sept. 1 expiration of a prior labor contract.

A strike remains a real possibility. And we have been conditioned by the pandemic and the war in Ukraine to expect the unexpected—and to expect the worst. But that instinct hasn’t been helpful when it comes to labor contract negotiations this year.

FIGURE 1. Very few steel mills achieved their stated objectives with price hikes announced in August.

We saw brinksmanship, negotiating past deadlines, and heated rhetoric in talks between Canadian steelmakers and USW over the summer. And more recently we saw the same between railroads and unions representing railroad workers. In each case, a deal was hammered out at the last minute. In other words, it was par for the course.

That’s not to say we couldn’t have a labor-related black swan with U.S. Steel and the USW this fall, or with union members not ratifying a tentative agreement. (Ratification votes at Cleveland-Cliffs, for example, are scheduled for October.) But I wouldn’t bet the farm on it.

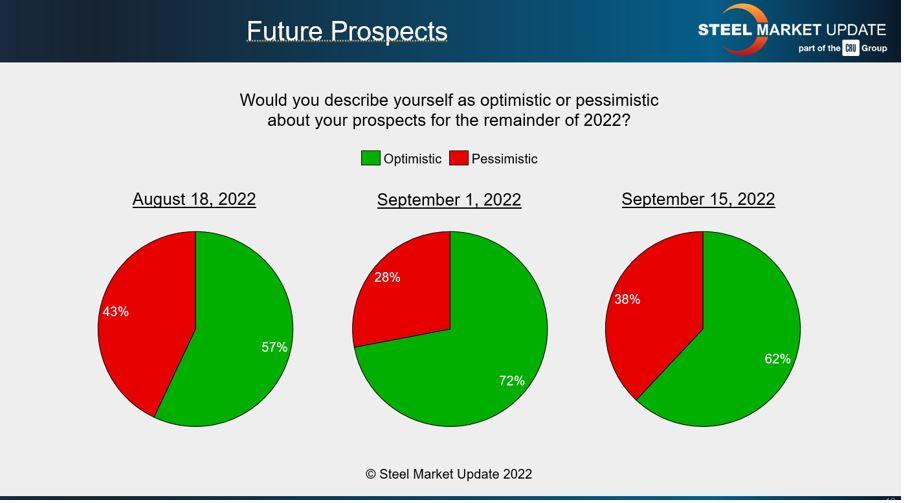

So, what about some of the softer indicators that are useful in providing context around the price? That’s where things might already be inflecting downward (see Figure 3).

I’d want to see another week of survey data showing worsening sentiment before I’d call it a trend. But it’s one to keep an eye on in the meantime.

That’s because that increase in pessimism is occurring against a backdrop of bearish real-world headlines. We just had Q3 guidancepalooza from U.S. mills. And it was not a pretty show.

Steel Dynamics Inc. (SDI) predicted lower Q3 earnings in part because of lower flat-rolled steel prices. It was a similar story at Nucor, which significantly lowered its Q3 earnings guidance in large part because of reduced margins and shipping volumes for sheet and plate.

U.S. Steel also forecast a much weaker showing in Q3, with earnings before interest, taxes, depreciation, and amortization expected to be down nearly 50% from Q2. The company also idled the No. 8 blast furnace at its Gary Works in Indiana on weak market conditions.

That move followed the idling of a tin line at Gary Works and a blast furnace maintenance outage that was pulled forward at the company’s Mon Valley Works in Pennsylvania. Pulling forward maintenance is something mills sometimes do to buy time in hopes of market conditions improving. The next step, if the market doesn’t turn upward, is often an idling.

I’m not saying that’s what’s happening at U.S. Steel, but again, it’s something to keep an eye on. Ultimately, such calls depend on profit margins (or the lack thereof) and supply/demand fundamentals.

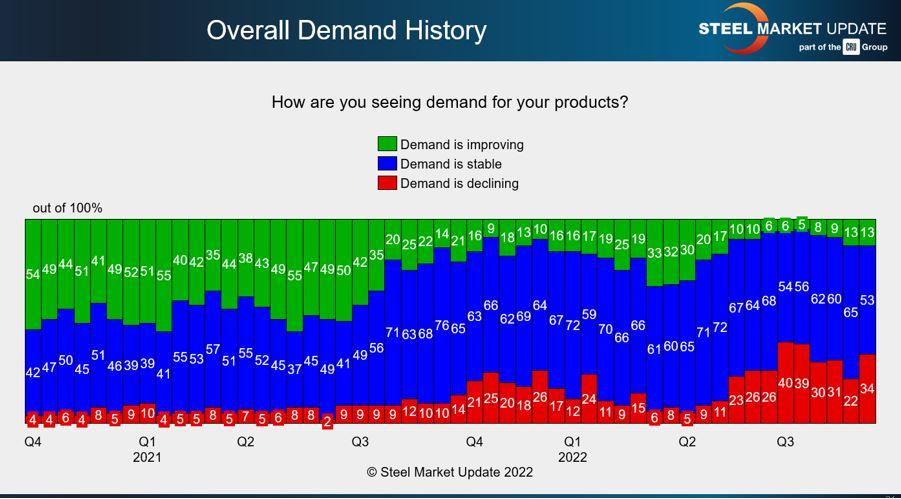

What about overall demand? After all, strong demand is the magic ingredient that makes volatility easy (or at least easier) to digest.

FIGURE 2. Most producers are willing to negotiate lower prices for sheet and plate, which makes it hard for them to achieve successful price hikes.

I had pinned some hopes on survey respondents reporting better or at least more stable demand. We had a welcome reprieve following a summer in which as many as 40% of respondents reported declining demand. But that brief trend of stable demand is now in question.

We’ve again seen a noticeable uptick in the number of people reporting declining demand—nearly 35% (see Figure 4). Again, one week of survey data does not make a trend. But I’d keep a close eye on this one, too, the next time we release full survey data on Sept. 30.

The next Steel 101 Workshop will be held on Oct. 19-20 in Corpus Christi, Texas. The highlight of the event will be a tour of SDI’s new steel mill in Sinton, Texas, the newest electric arc furnace sheet mill in North America. You can learn more at events.crugroup.com/steel101/about-steel-101.

We’re also well underway with planning for our Tampa Steel Conference on Feb. 5-7, 2023. It’s not too early to register, which you can do at www.tampasteelconference.com/registration.

If you want to participate in our survey, please contact SMU production manager and steel industry analyst Brett Linton at brett@steelmarketupdate.com.

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

In this episode of The Fabricator Podcast, Caleb Chamberlain, co-founder and CEO of OSH Cut, discusses his company’s...

{kind=link}