President/CEO

After an announced steel price hike, mills may have difficulty collecting the increase in the coming weeks. Getty Images

As of mid-November, steel prices appeared to be moving upward following price increases announced by the major flat-rolled and plate mills. Steel buyers and distributors now are wondering how high the prices might go and how long the price increase might last. The market was clearly split between those in a buying mode in anticipation of sustained higher prices and those in a wait-and-see mode, expecting yet another dead cat bounce.

On two occasions earlier this year, the mills raised prices only to see a soft, lifeless bounce, collecting a small increase for a short time and then watching the price of steel resume its downward trajectory. This time the flat-rolled mills announced one $40 increase on Oct. 24 and 25, then followed up with a second $40 increase on Nov. 7. Plate mills announced their own $40 price hikes in about the same time frame. Their goal is to reverse the 15-month downtrend that has nearly cut the price of steel in half, with serious consequences for sales and profits at mills and distributors alike. The benchmark price for hot-rolled has plummeted from more than $900/ton in the summer of 2018 to just $470/ton in mid-October, according to Steel Market Update (SMU) data.

It’s one thing for the mills to announce a price increase, but quite another for them to actually collect it. It generally boils down to the balance between supply and demand and how much support they get from service centers and distributors. Both are moving targets as the market approaches the end of the year.

Higher prices gained some traction in the first few weeks following the price hikes. The average price for hot-rolled steel moved up by $30 to $520/ton. Cold-rolled remained unchanged at $690/ton. The galvanized base price had a small $5 increase to an average of $695/ton. Galvalume® remained the same at $710/ton. Plate steel’s average price increased by $15 to $655/ton. Ferrous scrap prices, which have declined for much of this year, traded higher by $15-$25/gross ton in November, which promised to lend some support to higher finished steel prices.

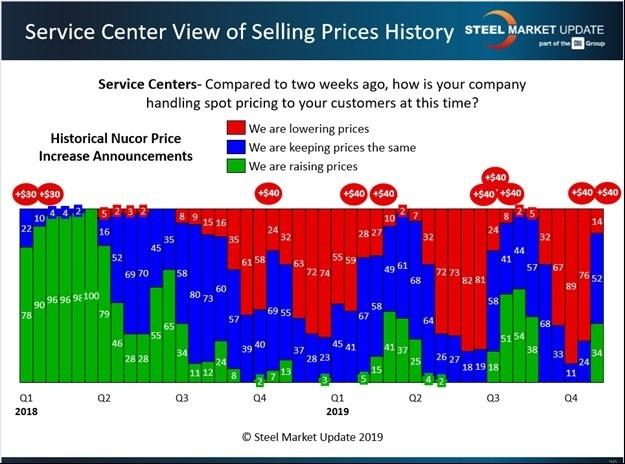

SMU anticipated the turnaround in prices as the market had been near the point of “capitulation” for several weeks. In tight, competitive market conditions, service centers often discount spot prices to win orders, even though they know declining prices erode the value of their inventories. The history of SMU data has shown that when at least 75 percent of distributors have been lowering prices, and the mills announce a price increase, the service centers will hit a psychological tipping point at which they capitulate and begin to support higher prices in pursuit of better margins. Figure 1 shows the two recent $40 price hikes in the circles to the right. It also shows that 89 percent of service centers were reducing prices to their customers just prior to the mills announcing the first increase.

What the chart does not show is how much support the mills will receive from distributors as they attempt to collect higher prices or how long before the service centers begin to discount once again. As illustrated by the red bars following the failed increases earlier in the year, the service centers were quick to begin reducing prices again. Perhaps predictive of the staying power of the latest price hike, only about one-third (34 percent) of the service centers polled last month said they were raising prices, while the majority (52 percent) were keeping prices the same.

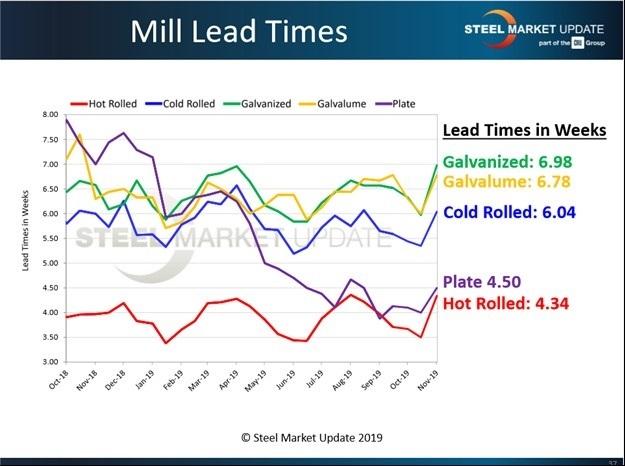

SMU also tracks lead times for steel delivery, which are a measure of demand at the mill level. Mill lead times for spot orders of flat-rolled showed signs of lengthening in November (see Figure 2). The average lead time for hot-rolled moved up to nearly four and a half weeks, cold-rolled to more than six weeks, and coated steels to nearly seven weeks. Thus, it appeared the mills were getting busier as buyers stepped up to place orders ahead of increasing prices. Rising prices and lengthening lead times seemed to indicate that demand was sufficient for the mills to collect at least a portion of the $80 increase they were seeking.

The state of negotiations between the mills and their customers is another key indicator that SMU monitors. Steel buyers are asked twice each month: Are the mills holding the line, or are they willing to discount the price to secure your order? It was no surprise that, following the price increases, negotiations between steelmakers and steel buyers tightened up a bit. What was surprising is that roughly two out of three buyers, as of the second week in November, still reported the mills actively negotiating spot prices on all types of steel products. This casts doubt on whether the mills will have the necessary discipline to stand behind their higher prices into next year or whether we are looking at the third dead cat bounce of 2019.

Here is some recent feedback from survey respondents about the recent price hikes:

On Jan. 7-8, 2020, Steel Market Update will conduct a Steel 101: Introduction to Steel Making & Market Fundamentals workshop in Fontana, Calif. The workshop will include a tour of the California Steel Industries mill.

Service centers appear to be responding to recent price hikes from the steel mills. Only 14 percent of the service centers surveyed recently indicated that they were still reducing prices. Steel Market Update

John Packard, president/CEO of Steel Market Update, can be reached at john@steelmarketupdate.com. Tim Triplett, executive editor for Steel Market Update, can be reached at tim@steelmarketupdate.com.

Steel Market Update’s mission with its newsletters, website, conferences, and educational programs is to inform, educate, and motivate those in the flat-rolled steel industry. For more information, visit steelmarketupdate.com.

Steel mills reporting lengthening lead times for their products appear to be supporting evidence that customers wanted to place orders before material prices rose any further. This creates an environment where the steel mills may be able to collect at least a portion of the $80 increase they announced in late October and early November. Steel Market Update

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

In this episode of The Fabricator Podcast, Caleb Chamberlain, co-founder and CEO of OSH Cut, discusses his company’s...