President/CEO

Steel prices jump in September, but many feel they will retreat in the coming weeks. Getty Images

Steel prices were on an upward trajectory entering the fourth quarter of the year. How high they will go, and for how long, is open to debate.

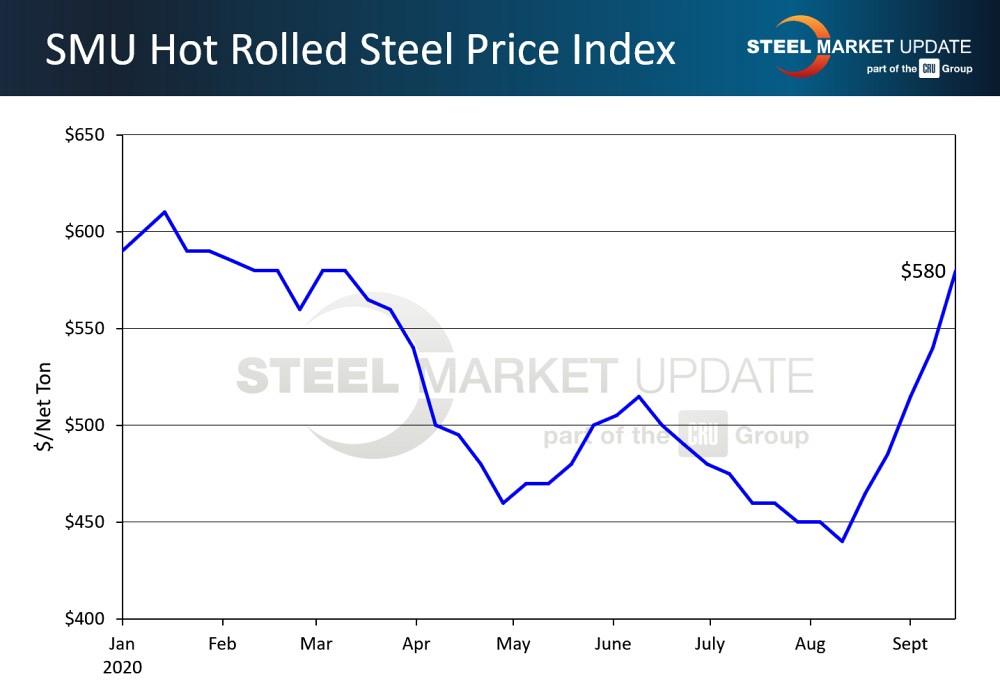

Steel Market Update’s survey of the market on Sept. 14-15 put the benchmark price for hot-rolled steel at $580/ton—back to the level it was in early March before the COVID-19 pandemic (see Figure 1). That’s up about $140 from the low of $440/ton reported by SMU in the second week of August. In mid-September, the same week as SMU’s survey, a few mills announced further price increases of $50/ton to $60/ton. Buyers were telling SMU that the mills were holding the line in price negotiations with $600/ton as the target for hot-roll.

Will they be able to collect it? There are two schools of thought, captured well by contrasting quotes from two SMU sources:

Bank of America Analyst Timna Tanners raised her second-half steel forecast to reflect the better-than-expected demand behind the price increases, but her outlook was cautious.

“U.S. hot-rolled coil prices are heading for $600/ton near term, with Monday's price hike supported by higher scrap costs for mini-mills and strong auto demand tying up their integrated mill peers. We expect near-term strength that can last into November, as recent greater protection from imports and strong Chinese demand keep global alternatives expensive.”

She pointed to mill outages that tightened supplies, including planned downtime at Stelco's Hamilton mill, reduced volumes at NLMK's Farrell, Pa., mill due to a strike, and unplanned outages at U.S. Steel's Mon Valley and ArcelorMittal's Burns Harbor. “However, we expect disrupted mills to resume output and seasonal weakness in Q4 to dampen prices ahead,” she said.

Back in the spring, when the government shut down much of the economy to stem the spread of COVID-19, numerous mills idled furnaces and cut production to sync with the curtailed demand. Much of that capacity is back online, but not all. Additionally, some outages still are planned for the fourth quarter. Some experts believe the escalating steel prices are as much about the tight steel supplies as about growing demand.

“Demand is improving for sure at the margin, but this is really a supply-side squeeze and those tend to be short-lived,” said KeyBanc Analyst Phil Gibbs.

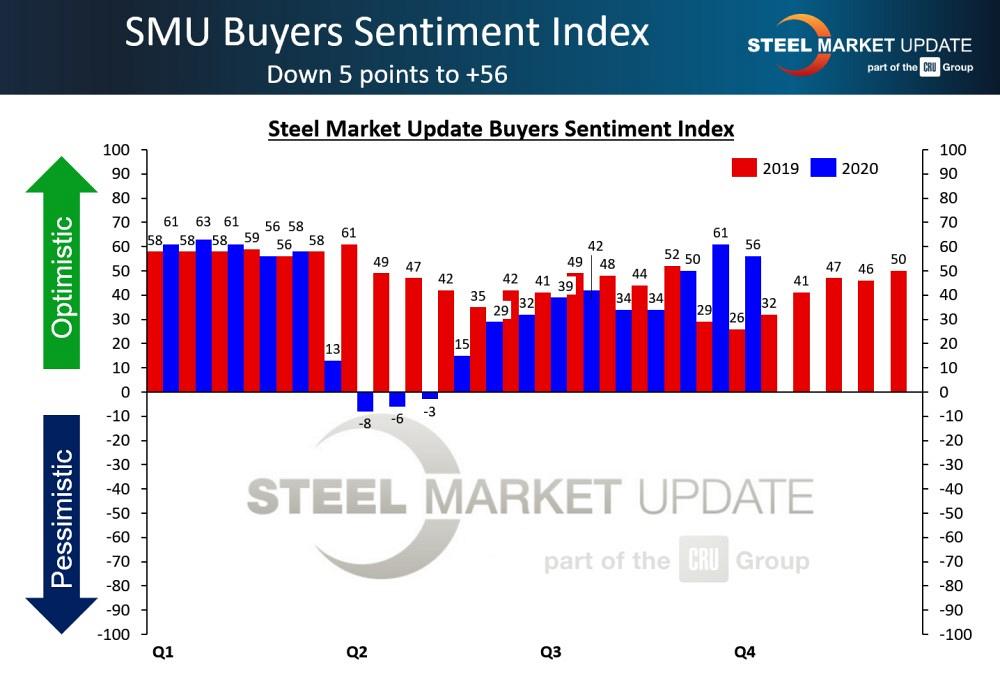

While the economy and the steel market have a long way to go to recover from the ongoing pandemic, the steel industry sees reason for optimism. Steel industry sentiment has rebounded to levels even better than this time last year. SMU’s Steel Buyers Sentiment Indexes have been improving in fits and starts since hitting bottom in early April. That optimism sends a message about the potential staying power of higher steel prices in Q4.

Every two weeks SMU asks steel buyers how they view their company’s chances for success in the current environment and three to six months in the future. The current sentiment reading in the survey taken the week of Sept. 14 was +56, up from a weak +26 at this time last year and a substantial rebound from the low of -8 in the first week of April, its lowest reading since November 2010 (see Figure 2).

Figure 1. Hot-rolled steel prices are creeping back to where they were just before the coronavirus crisis hit the U.S.

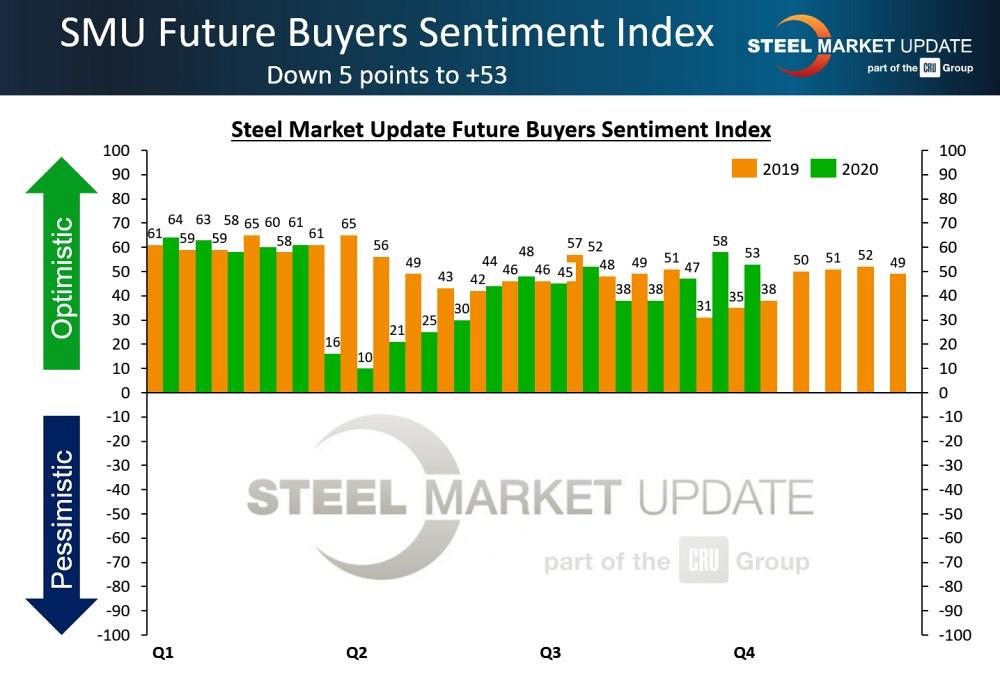

SMU’s Future Sentiment Index had a reading of +53, an improvement from the +35 in September 2019, when the hot-rolled steel price was under $500/ton (see Figure 3). Future Sentiment hit a recent low of just +10 in early April shortly after the pandemic took hold.

SMU also asked readers in mid-September: Looking ahead, do you feel upbeat about your company’s prospects in the fourth quarter? More than 75% said they are looking forward to a strong finish to the year. Here are some of their comments:

Buyers still have some concerns. These comments help to describe some of the main points of worry:

SMU provides real-time pricing, news, and analysis of market trends affecting North American flat-rolled steel, plate, scrap, and related markets. To sign up for your free three-week premium trial, email paige@steelmarketupdate.com, or call 724-720-1012.

John Packard, president/CEO of Steel Market Update, can be reached at john@steelmarketupdate.com. Tim Triplett, executive editor for Steel Market Update, can be reached at tim@steelmarketupdate.com.

Steel Market Update’s mission with its newsletters, website, conferences, and educational programs is to inform, educate, and motivate those in the flat-rolled steel industry.

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

In this episode of The Fabricator Podcast, Caleb Chamberlain, co-founder and CEO of OSH Cut, discusses his company’s...

{kind=link}