President/CEO

Fabricators and manufacturers may find some bargains on raw materials in the fourth quarter as spot steel prices continue to moderate and service centers look to reduce their higher-cost inventories.

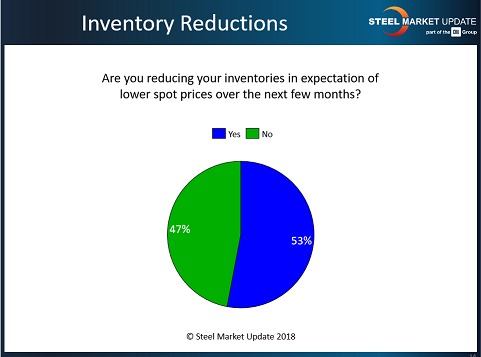

Flat-rolled market surveys from Steel Market Update (SMU) show that service centers are in the process of working down their inventories in response to declining prices and softening demand (see Figure 1). Flat-rolled steel distributors now average 2.6 months of supply on hand, down from 2.7 months at the end of July, according to SMU proprietary data.

Spot prices in the market appear to be correcting from near-historic highs on weaker demand in some sectors. In the past three months, the price of hot-rolled steel has declined by about 9 percent. Service centers report that many customers are buying only for their immediate needs and postponing large orders in anticipation of cheaper steel in the months to come.

In the past year the benchmark price for hot-rolled steel jumped by more than 50 percent, from a low of $615 per ton last October to a high of $930 per ton on June 1. Spot prices in the U.S. got a major boost from the 25 percent tariff on steel imports first announced by the Trump administration in March. As a result, steel imports into the U.S. have declined by about 10 percent this year, compared with the same period in 2017.

SMU regularly canvasses the flat-rolled steel market. Following were SMU’s benchmark steel prices, FOB the mill east of the Rockies, as of Sept. 18:

Steel plate is the exception. Plate supplies were tight with upward price momentum as plate mills remained on controlled order entry. SMU’s price range on steel plate was $980/ton to $1,030/ton ($49.00/cwt to $51.50/cwt) with an average of $1,005/ton ($50.25/cwt) FOB the customer's facility for orders to be delivered during the month of November. Plate lead times for allocations were seven to 10 weeks.

Domestic flat-rolled and plate mills are operating near full capacity. In the week ending Sept. 15, the industry hit an average capability utilization rate of 79.4 percent, within striking distance of the 80 percent level the industry says it needs for sustained profitability. That percentage includes idled capacity and slower long-product fabrication, which makes it misleading. Major flat-rolled mills are operating well above the 90 percent level. U.S. crude steel production for the year to date was up 4.3 percent, according to the American Iron and Steel Institute.

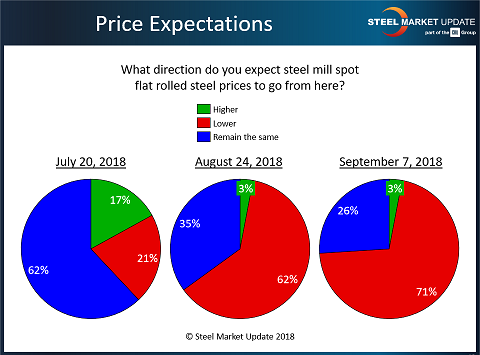

Whether the current downtrend in steel prices is temporary or will continue into next year depends on a number of factors (see Figure 2). On the political front, the Trump administration is engaged in a tit-for-tat trade war with China that goes far beyond steel. The U.S. has imposed three rounds of tariffs on various Chinese products this year totaling $250 billion and has threatened an additional $267 billion in tariffs if China retaliates further. If negotiations with China fail, the U.S. possibly could subject virtually China’s exports to the U.S. to duties next year. That has serious implications for consumer prices, the growth of the U.S. economy, and steel demand.

Also factoring into steel prices is the cost of ferrous scrap that is remelted by steel producers. The benchmark price of shredded scrap peaked in April at about $390/ton but has since declined to around $340/ton, contributing to the recent dip in steel prices.

Another wildcard to keep an eye on are the negotiations between the United Steelworkers (USW) and the nation’s two largest integrated steel producers, U.S. Steel and ArcelorMittal. The contract talks could become especially contentious as the two sides debate how to split the big gains the mills have enjoyed as a result of President Trump’s steel tariffs. Ironically, contract negotiations when the mills are reporting record profits may prove more difficult than in the past when the mills were struggling and seeking concessions from the union. USW members have authorized the union to strike, if necessary, to ensure that the workers get their fair share of today’s windfall. A work stoppage at one or both mills could tighten steel supplies and boost steel prices fairly quickly.

Figure 1. Steel service centers are looking to clear out their high-priced inventories in the face of what is expected to be reduced customer demand.

On Dec. 11-12 SMU will conduct another one of its “Steel 101: Introduction to Steel Making & Market Fundamentals” workshops in Toledo, Ohio. Attendees will tour North Star BlueScope’s electric-arc furnace and rolling mills.

Information about any of these workshops can be found at www.steelmarketupdate.com/events.

Figure 2. Steel consumers expect flat-rolled steel prices to fall in the coming months.

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

Seth Feldman of Iowa-based Wertzbaugher Services joins The Fabricator Podcast to offer his take as a Gen Zer...