Senior Editor

Even with the threat of a steel strike or lockout at U.S. Steel, most steel buyers are confident that hot-rolled steel prices won't spike in the near term. Kapook2981/iStock/Getty Images Plus

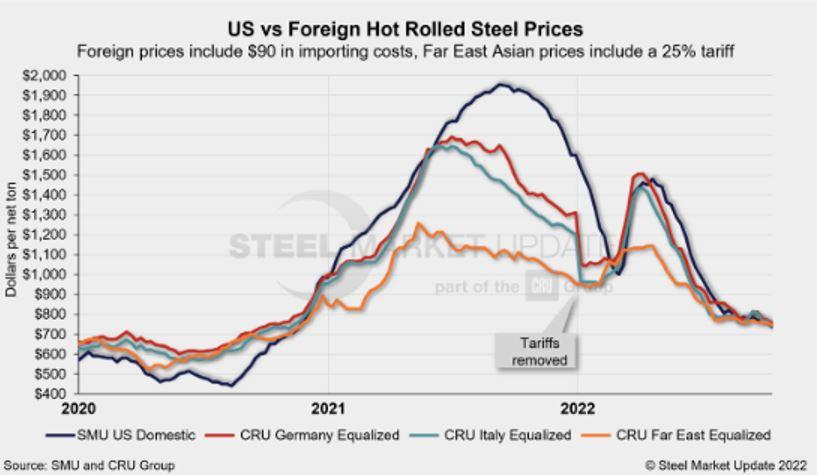

It’s time for a contrarian moment. Sentiment is increasingly bearish after months of falling steel and scrap prices, uneven demand, increased capacity, and rising interest rates. That said, imports are down, and apparent steel supply is at its lowest since February. Also, imported hot-rolled coil (HRC) costs—once you account for freight, trader profit margins, and tariffs, among other things—are modestly higher than domestic prices (see Figure 1).

What if something unexpected happens—a strike, an unplanned outage, or another black swan? What if buyers, on the sidelines now, jump back into the market all at once?

I’m not saying the market is going to catch fire. It’s possible prices keep sliding downward. But it’s also worth considering whether the forest is dryer now than it’s been in a while.

What might that spark be? There has been speculation in both the physical and futures markets that a strike or lockout at U.S. Steel could catch buyers off guard and send prices spiraling upward.

Also, you could make a case that the chance of a strike or lockout increases the longer talks drag on between the Pittsburgh-based steelmaker and the United Steelworkers (USW).

Recall that a prior agreement expired on Sept. 1. The USW already has agreed to new labor contracts with Cleveland-Cliffs and with Canadian flat-rolled steelmakers Stelco and Algoma. That leaves the U.S. Steel talks as the only one that has yet to resolved.

While I might be feeling contrarian, most respondents to our surveys don’t see trouble on the horizon and continue to predict that steel prices will remain on the downward trajectory they’ve been on since mid-May, following a spike upward after the Russian invasion of Ukraine. Most don’t anticipate talks between U.S. Steel and the USW breaking down (see Figure 2).

I’ve talked to U.S. Steel customers who have said that company sales representatives have dismissed heated rhetoric from the USW as just bluster. It is notable that the union in recent updates to members has subtly shifted its language from saying that there has been “no significant movement” to more recently saying that there has been “some progress.”

What did survey respondents have to say about a potential strike or lockout at U.S. Steel?

Still, I think it’s worth thinking about a few things if a strike or lockout were to occur:

Figure 1. Domestic prices for hot-rolled coil remain slightly below that of imported product.

The majority thinking that a strike or lockout at U.S. Steel won’t occur partly explains why many buyers no longer think that prices have bottomed (see Figure 3). In our last full survey in late September, 27% of respondents said they thought prices already had bottomed. Now, only 9% think that. The most common response now is that prices won’t bottom until November.

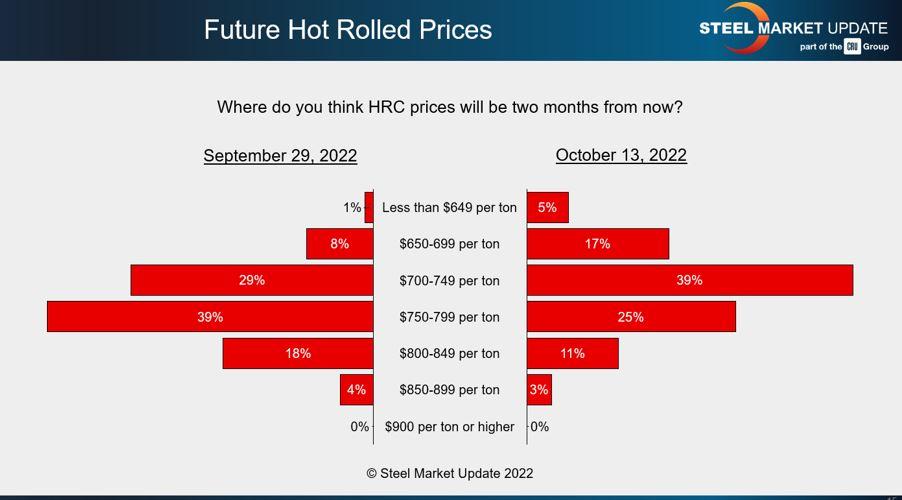

We’ve also seen survey respondents lower their expectations for HRC prices (see Figure 4). Back in September, 39% of survey respondents predicted that HRC prices would be $750/ton and $799/ton two months later. Now, 39% think prices in two months will be in the range of $700/ton to $749/ton.

Also notable is that we’ve seen a significant increase in the number of people predicting that prices will fall below $700/ton. Twenty-two percent of respondents think that threshold will be broken now, up from just 9% in our last survey.

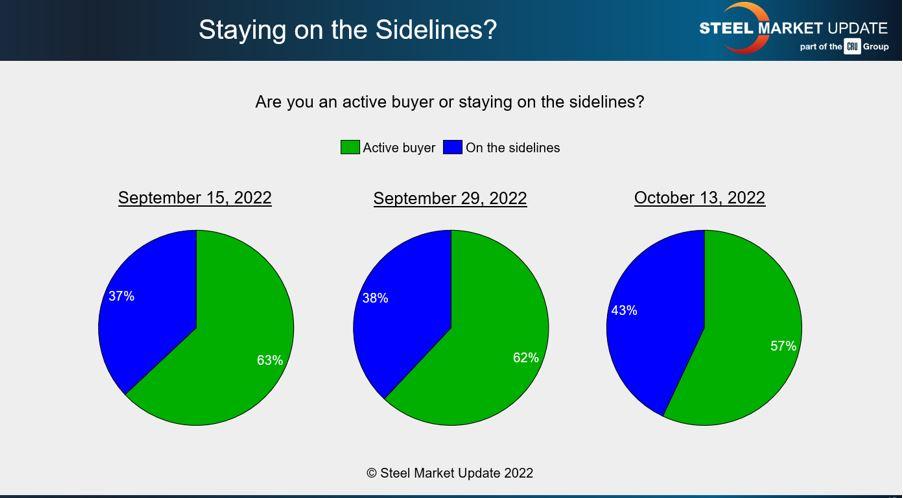

Probably because steel consumers expect prices to continue to decline, many remain on the sidelines (see Figure 5).

Many report that they aren’t buying or are only buying as needed. Here are a few representative comments from our survey:

But that opinion is not unanimous. Some steel consumers remain busy. “I have to buy because I am as low as I have ever been on coil,” said one steel buyer.

We’ll be keeping a close eye on prices, lead times, mill negotiations, and sentiment in our next survey for any signs of an inflection point. Those survey results will be available on Oct. 28.

Steel Market Update’s next training workshop, Introduction to Steel Hedging: Managing Price Risk, will be held on Nov. 30 – Dec. 1. It’s a good way to learn about futures, which are an increasingly important part of the steel market. The workshop is virtual. You can learn more about the event and register here.

Don’t forget to mark Feb. 5-7 on your calendar. That’s when we’ll be holding our Tampa Steel Conference in conjunction with the Port of Tampa Bay. This in-person event in Florida is a growing event, and it’s a great reason to get out of the cold and catch up with hundreds of your closest friend in steel. You can register here.

If you want to participate in our survey, please contact Steel Market Update production manager and steel industry analyst Brett Linton at brett@steelmarketupdate.com.

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

Seth Feldman of Iowa-based Wertzbaugher Services joins The Fabricator Podcast to offer his take as a Gen Zer...

{kind=link}

{kind=link}

{kind=link}