Certified Public Accountants

Your company can be rewarded by saying “yes” to difficult projects.

On Dec. 16, the U.S. Congress announced the passage of the tax bill, Protecting Americans from Tax Hikes (PATH) Act of 2015. This long-awaited tax legislation made permanent some important income tax deductions and credits related to businesses. One of the benefits made permanent was the research and development (R&D) tax credit. This credit rewards companies for time spent solving product and manufacturing problems.

The R&D tax credit originally was enacted in 1981 to encourage U.S. companies to improve their competitiveness. In 2001 President George W. Bush recognized that the credit was not being used because of the high innovation thresholds contained in the law. As a result, the R&D tax credit law was amended to lower the qualifying thresholds so that more companies could receive benefits.

The credit has had a bumpy ride since 1981. It expired after its initial four and a half years and was renewed on a year-by-year basis until December 2014. With the passage of the PATH Act, qualifying companies can rely on this benefit for many years.

The question now: What does it take to qualify?

When you think of R&D, your thoughts automatically turn to lab coats and scientists. That might have been the case in 1981, but it is no longer the standard.

To understand how a fabricator can qualify for the R&D tax credit, let’s consider a very familiar scenario. A customer presents a shop with a rough sketch of a part and asks the fabricator to accept the job. In this case, the fabricator has never made the part. The quantity, which could be one or 1 million, is irrelevant as it relates to the R&D tax credit.

The owner or the manager of the fab shop should consider these questions, which help to determine if the work associated with the new job might qualify for the tax credit:

A fab shop can meet this qualification even though the customer designed the part. When a fabricator quotes a part, it is not being paid directly for the development time associated with the part; a customer just wants the shop to produce the part that meets its specifications. The government, however, is interested in rewarding the fab shop’s risk with the tax credit. The idea is that the shop maintains more of its cash, which it can use to grow the business.

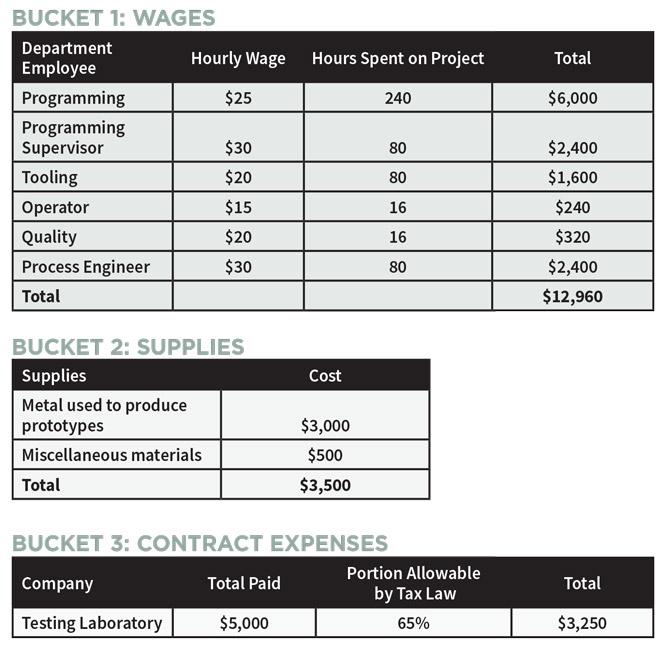

Once a fabricator can determine what activities might qualify for the R&D tax credit, it needs to know how to proceed. There are three buckets—or as the tax law calls them “qualified research expenditures”—that R&D costs can be put into: wages, supplies, and contract expenses. The expenses stop accumulating as soon as a part is ready for commercial production. In other words, when the first part has passed quality checks and the customer has accepted the part, the shop can no longer claim additional expenses and apply them to the tax credit.

Wages normally are the largest expense. It includes gross pay of the employees that spent time on the project, meeting the four tests previously mentioned. The expense is calculated by multiplying each employee’s gross pay rate by the hours spent on the R&D project. If the employee is salaried, then the company could use the percentage of total work time spent on the R&D project.

Supplies include the material used to produce prototypes or first articles. Typically, this includes the raw material, components, fasteners, and paint.

Contract expenses include any third-party testing or engineering services. There are two stipulations:

If a fabricator pays an engineering firm a fixed fee for its service, the IRS considers the engineering firm financially responsible, and the fabricator cannot include this cost in its R&D tax credit calculation. However, if a fabricator pays the firm on an hourly basis, then the fab shop is eligible to claim this cost. As a result, it is a good practice to tailor these agreements on an hourly basis with a cap. This ensures that a fabricator can include the costs in its R&D tax credit calculation and is protected from surprise charges.

To fully illustrate how the R&D tax credit can be applied in a manufacturing setting, let’s look at an example. A shop wins a job, and the customer sends it a model for an airplane part. This part requires a hinge that will be difficult to machine because of thickness specifications. (Keep in mind that the customer is not paying the shop to solve this machining problem; it just wants the shop to build the part.)

The qualified research expenditures might look like this:

That’s $19,710 that can be applied to the R&D tax credit. That shop would be doing itself a disservice by not exploring this cost-saving opportunity.

Is your shop missing out?

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

In this episode of The Fabricator Podcast, Caleb Chamberlain, co-founder and CEO of OSH Cut, discusses his company’s...