President/CEO

Steel mills are getting steel deliveries to customers much more quickly than they were in the summer. That's good news steel users. Getty Images

Steel prices are falling fast—so fast that we hesitate to put numbers to paper for fear they’ll be old by the time the ink dries.

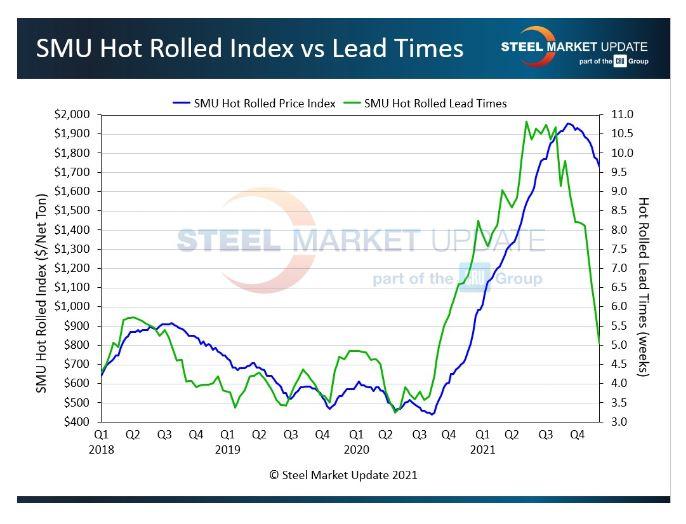

Why are we almost certain prices will continue to drop? Lead times lead steel prices on the way up and on the way down. (Recall that lead times are the time between when an order is placed at a mill and when that order is processed.) That’s why Steel Market Update (SMU) keeps just as close an eye on lead times as on prices.

And prices have a lot of catching up to do on the downside, if Figure 1 is any indication. As of Dec. 7, SMU’s average hot-rolled coil (HRC) price was $1,730/ton ($86.50/cwt). That’s down about 7% from $1,855/ton last month and down nearly 12% from a 2020 peak of $1,955/ton in early September.

Talk of gradual declines began just weeks ago. That’s not the case anymore. And in any other cycle, a decline of $225/ton in just a few months would have been catastrophic. But it shouldn’t have caught you by surprise if you were paying attention to lead times.

Hot-rolled lead times now average about five weeks, down from an average of approximately seven weeks in November—and a far cry from the 10 to 11 weeks over the summer. Actually, we’ve seen published hot-rolled lead times from some mills as short as three to four weeks—or about 67% lower than the peak.

In other words, some mills still have (or recently had) tons available before the end of the year. That’s not unheard of this time of year in a normal market, but it’s a huge change from earlier this year when buyers were on allocation and when lead times could be measured in months. What’s even more notable is that galvanized lead times at some mills are the same or even shorter than HRC lead times. That’s not something you see very often.

There is not a one-to-one correlation between prices and lead times. Lead times vary widely by mill. And the 67% decline noted above is arguably extreme and too back-of-the-napkin to be useful. But we think the scenario is at least worth pondering. Because it would suggest that if prices mirror lead times, they could fall approximately $1,300/ton from their peak, which would put the price for HRC at $655/ton.

That’s alarmist, we know. Again, it’s just food for thought. We’d also point out that $655/ton is not a bad price by historical standards.

But further downward movement seems inevitable. As this was being written in early December, we had confirmed deals in the $1,600/ton range. That’s still well above import prices, with Italian and German HRC in theory about $400/ton to $500/ton less expensive than U.S. material, per SMU calculations.

Germany, the European Union’s biggest steelmaker, is not known for cheap steel. And that spread matters more than it used to because blanket Section 232 tariffs of 25% come off the EU effective Jan. 1. It also appears the EU tariff rate quotes could serve as a template for similar deals with other U.S. allies, such as the U.K., Japan, and South Korea.

Figure 1. As lead times for steel go, so do steel prices. The precipitous drop in lead times from the steel mills indicates that steel prices might be headed the same way.

Long gone from the market is talk of HRC hitting $2,000/ton. The question now is where prices will bottom. Most agree it’s probably going to be substantially higher than the $400/ton to $500/ton floors we’ve seen in past down cycles.

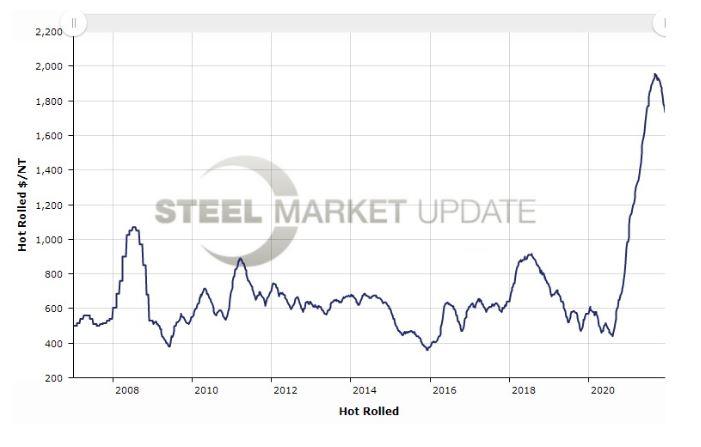

By the way, if this last year feels like it’s been a little overwhelming, that’s because it has been (see Figure 2).

The bumps on the road here are the run-up to the 2008 financial crisis, when HRC prices hit what was then an unprecedented high of $1,070/ton. Another bump is the spring/summer of 2018, when Section 232 tariffs were rolled out by the Trump administration, catching even some domestic steelmakers by surprise and sending prices soaring upward.

Those were big events that garnered big headlines around the world. But they pale in comparison to what we’ve experienced over the last year as demand snapped back following the outbreak of the COVID-19 pandemic.

Most of us have never experienced a market like this. It’s unlikely we will again anytime soon. Let’s just hope the ride down isn’t as sharp as the ride up. But let’s also plan for the possibility that prices took the stairs up and are taking the elevator down—assuming they don’t jump off the roof.

The saving grace to all of this: End-use demand is good. And almost everyone made good money over the last year.

No, there is no more rush to secure steel—no more double and triple ordering. But this isn’t 2008. The music hasn’t stopped. It’s just no longer blaring so loudly that it’s waking up the entire neighborhood.

With times as volatile as they are, you’re going to want to know what your peers and industry experts are thinking. A great way to find out is by attending the Tampa Steel Conference, which is co-hosted by SMU and Port Tampa Bay. The event will be held live on Feb. 14-16 at Tampa’s Marriott Water Street Hotel. You can learn more about the agenda, speakers, costs to attend, and how to register here.

In the meantime, check out our Steel 101 Workshop, which will be held virtually on Jan. 11-12. It’s great for those new to steel and for industry veterans who could use a refresher on the basics. Information on the agenda, instructors, and costs is available here.

Figure 2. The steel price increases of 2021 make the spikes in 2008 and 2019 look quaint.

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

In this episode of The Fabricator Podcast, Caleb Chamberlain, co-founder and CEO of OSH Cut, discusses his company’s...