President/CEO

The benchmark price for hot-rolled steel peaked at this time last year at around $910/ton but declined by 40 percent in the second half of 2018 and first half of 2019.

As of mid-July, after a yearlong downtrend, steel prices appeared to have finally turned around. Whether the uptrend has legs or will be short-lived will reveal itself in the coming weeks.

Mills and service centers suffered a serious margin squeeze in the past year as they watched steel prices, and the value of their inventories, decline week after week. Last year’s jubilant announcements of mill expansions and upgrades have given way to idled furnaces, capacity reductions, and questions about true steel demand.

The benchmark price for hot-rolled steel peaked at this time last year at around $910/ton but declined by 40 percent in the second half of 2018 and first half of 2019 despite the Trump administration tariffs that limit the competition domestic steelmakers face from imports.

Steel Market Update (SMU) data indicates hot-rolled prices appeared to bottom out in the first week of July at around $520/ton, but then increased by $30 following two $40 price increase announcements by the major mills. The market may not accept the entire $80 increase right away, but the mills seem to be collecting at least a portion of it, which means higher prices for manufacturers and fabricators.

SMU gathers real-time pricing data from steel buyers every week. The price direction, as represented by SMU’s Price Momentum Indicator, had been pointing “lower” for most of the past year. So it was a noteworthy event when SMU moved its momentum indicator to “higher” on July 12.

At that time, according to SMU data, the benchmark price for hot-rolled steel (FOB the mill, east of the Rockies) was averaging $550/ton ($27.50/cwt), with lead times that had stretched a bit to three to five weeks. Cold-rolled averaged $710/ton, with lead times of four to seven weeks. The price for benchmark galvanized 0.060-inch G90 coil averaged $798/ton, with a five- to seven-week lead time for spot orders.

Price momentum for plate steel continued to trend “lower,” with the delivered price for plate averaging $780/ton ($39/cwt), with lead times of three to six weeks.

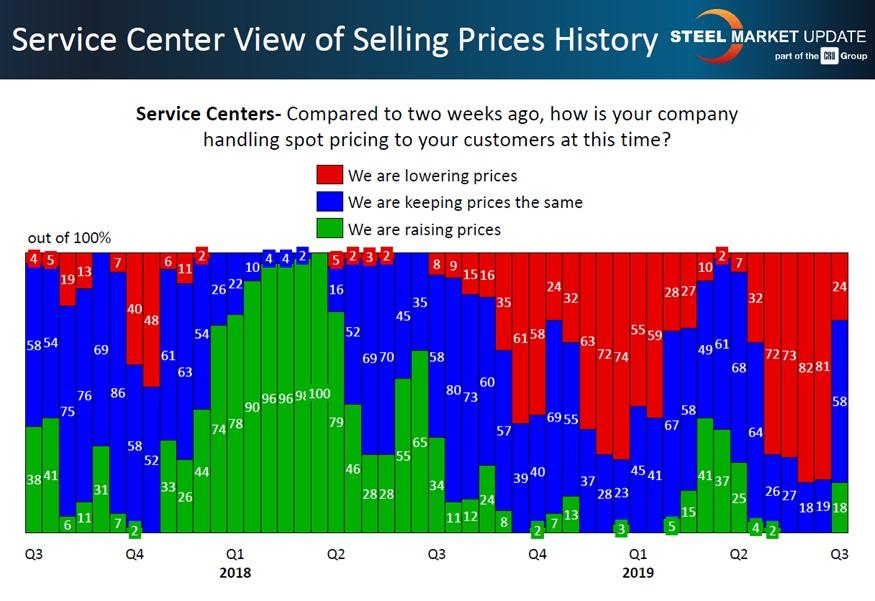

Other SMU market data supports the change in momentum. SMU sends out a market trends questionnaire to steel buyers every two weeks, and the shift in the pricing direction was evident in the last batch of returns. As seen in the bars on the far right in Figure 1, just 24 percent of service centers said they were still reducing spot pricing for their customers, down dramatically from 81 percent in the prior canvass. Perhaps the leading predictor of whether mill price hikes will “stick” is how much support they get from service centers. The fact that the majority of service centers (58 percent) said they were still keeping prices the same, rather than raising them, suggests that many remained unconvinced the turnaround was yet for real.

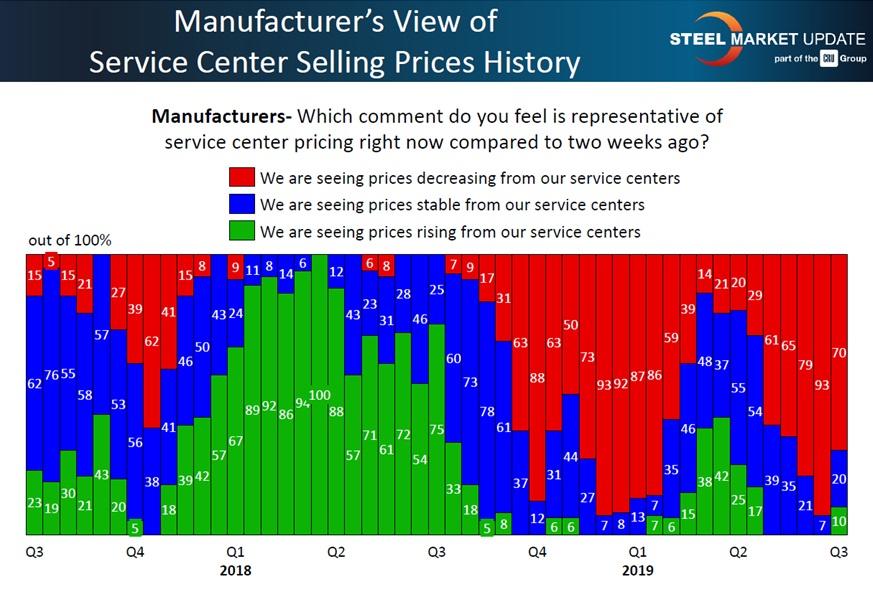

Seventy percent of the manufacturers responding to SMU in the first week of July (see Figure 2) reported that spot pricing from their distributors continued to move lower—still a high percentage, but 23 percentage points fewer than reported in mid-June prior to the mill price increase announcements.

SMU will be watching the green bars in these graphics carefully from this point forward. For the mill price increases to gain traction, the distributors need to begin raising spot prices to their customers. Earlier this year the market experienced a “dead cat bounce.” (Even a dead cat will bounce if dropped from a high enough height.) This can clearly be seen in the green bars during the latter portion of first-quarter 2019. Service center prices rose briefly, then receded. If the latest mill increases receive the same tepid support, the long-awaited rebound for steel may suffer the same fate as that poor cliched kitty.

After months of holding the line on price increases, 18 percent of service centers surveyed reveal that they are raising prices as of mid-July. Many industry observers wonder if this trend will continue or if it is short-lived.

Opinions are split among steel buyers on whether demand will be sufficient to sustain higher steel prices in the second half. Some fear another bounce in which the turnaround proves only temporary.

Here are some anonymous responses about a temporary price bounce that we received from steel buyers:

On Oct. 8-9, Steel Market Update will conduct its next Steel 101: Introduction to Steel Making & Market Fundamentals workshop in Cincinnati. This workshop will include a tour of the Nucor Steel Gallatin Mill.

Only a small percentage of manufacturers indicate that they have witnessed service centers charging more for steel.

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

Seth Feldman of Iowa-based Wertzbaugher Services joins The Fabricator Podcast to offer his take as a Gen Zer...