President/CEO

With more sidelined steelmaking capacity returning to action and new capacity opening up in 2021, steel mills might find that supply might outstrip demand for steel in the coming year. That's good news for metal fabricators. Getty Images

With more steelmaking capacity set to come online soon and steel demand likely encountering some weakness, rising steel prices could be near their 2020 peak. Steel prices may well trend lower in 2021, according to experts.

Steel Market Update’s check of the market on Oct. 12-13 showed a base price for spot orders of hot-rolled steel of $650/ton. That benchmark hot-rolled price began the year at $610/ton and was at $580/ton in March when COVID-19 hit. Government-ordered shutdowns to stop the spread of the virus took a big toll on the economy and steel demand, driving the steel price down by more than 20% in just six weeks. Hot-rolled steel had a low for the year of $440/ton in mid-August.

Certain segments of U.S. manufacturing have made a surprisingly strong recovery since then. Auto production is back to its pre-pandemic pace. Construction activity has been robust, though residential is much stronger than the more steel-intensive commercial construction. Most other steel-consuming sectors have made a comeback to some degree or another, except for energy which remains in the doldrums.

The steel price story is not all about demand, though. Beginning in May, a series of price hikes by the mills managed to boost steel prices by more than $200/ton. Mills that dialed back production due to the pandemic have taken their time restarting idled furnaces. Planned maintenance outages, and a few notable unplanned outages caused by equipment failures, have kept steel supplies tight, relative to demand. Thus, the recent increase in prices has been at least partially supply-driven.

Bank of America calculates that some 9.4 million tons of steelmaking capacity was temporarily closed, and most of it will return to the market at some point. More than 10 million tons of new production is planned to come online in the next two years, including a doubling of capacity at Big River Steel in Arkansas, Steel Dynamics’ new mill in Texas, Nucor’s new plate mill and expansion in Kentucky, and ArcelorMittal’s new slab mill in Alabama. Bank of America Analyst Timna Tanners maintains that all this new capacity threatens to throw supply and demand so badly out of balance that the market is facing a glut that will drive steel prices to dangerously unprofitable levels, a phenomenon she has dubbed “Steelmageddon.” Currently, Bank of America forecasts hot-rolled steel prices will average $490/ton in 2021 and $475/ton in 2022 as new capacity puts downward pressure on prices.

Raising eyebrows was the Sept. 28 announcement that mining company Cleveland-Cliffs was planning to acquire most of ArcelorMittal USA, after purchasing AK Steel earlier in the year. The two acquisitions make Cliffs the largest flat-rolled steel producer in North America. Cliffs now holds a unique competitive position in the market as a vertically integrated steel producer, supplying raw materials to its own integrated mills, which are among the biggest suppliers of flat-rolled steel to the U.S. auto industry. Because of its massive scale, Cliffs is also in a position to influence the steel supply and perhaps keep Steelmageddon from being such a disaster.

SMU data shows that service center inventories were at record lows in September, while product on order was at record highs. Some suggest that service centers may have waited too long to replenish their inventories, and then overbought to stay ahead of further price increases, pulling demand forward. The net result is likely to be reduced demand from the distribution sector into first-quarter 2021 as service centers work down high stock levels.

Mills reportedly are pushing for $700/ton for hot-rolled, but only 27% of buyers surveyed by SMU last month believe prices will get that high before correcting. About 38% believe steel prices are already peaking around the $650 level.

The amount the mills must pay for ferrous scrap, which is remelted to make new steel, factors heavily into what they charge for their steel products. Scrap prices rose in August and September, but traded sideways in October. They were expected to be flat to down in November and December, further impacting finished steel prices.

So, in summary, there are several reasons to believe that steel prices are likely to trend lower:

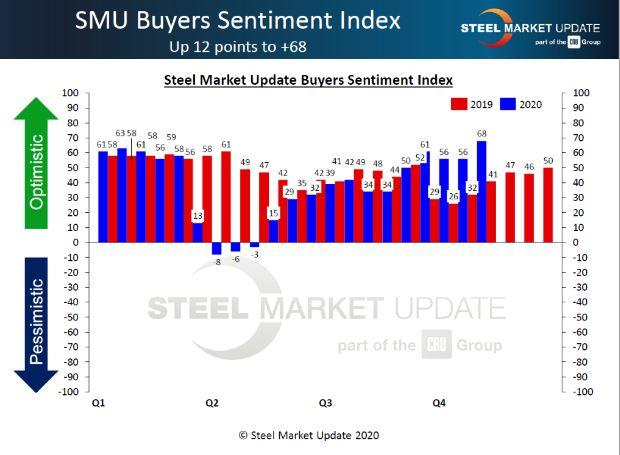

Figure 1. Steel buyers’ optimism is as strong as it’s been at any time this year.

Industry sentiment, as measured by SMU, remained surprisingly positive last month, given all the uncertainty over the election and the spread of the coronavirus. Every two weeks, SMU asks steel buyers how they view their company’s chances for success in the current environment. The current sentiment reading was +68 in mid-October (see Figure 1). Compared with the first week of April, when the coronavirus effect was at its worst at a reading of -8, that’s a 76-point swing. Current sentiment is much healthier than at this time last year when it registered a weak +26, reflecting disappointing hot-rolled steel prices of $500/ton.

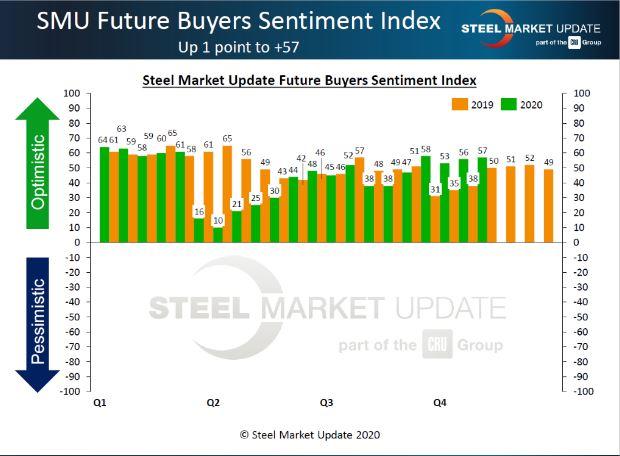

SMU also asks buyers how they view their company’s chances for success three to six months in the future. SMU’s Future Sentiment Index registered +57 (see Figure 2), a 47-point rebound from the low of +10 shortly after the pandemic hit. At this time last year, future sentiment registered a pessimistic +35. The fact that respondents were less optimistic about the future, polled just weeks before the election, was no doubt affected by the acrimonious presidential election.

Steel buyers have mixed views on the sustainability of steel demand and the likelihood the mills will continue to collect higher prices. In a poll last month, SMU asked: “Do you think the mills will be able to collect the latest price increases on flat-rolled and plate products? Do you share some industry executives’ concerns that the U.S. steel market is on track for a severe shortage of supply?” Here’s what some executives had to say:

Not a Steel Market Update Subscriber?

SMU provides real-time pricing, news, and analysis of market trends affecting North American flat-rolled steel, plate, scrap, and related markets. To sign up for your free three-week premium trial, email paige@steelmarketupdate.com, or call 724-720-1012.

Figure 2. Steel buyers’ future sentiment is tempered somewhat by the ongoing effects of the coronavirus crisis, but it is markedly better than it was when the pandemic first began early in the second quarter.

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

In this episode of The Fabricator Podcast, Caleb Chamberlain, co-founder and CEO of OSH Cut, discusses his company’s...