Principal

U.S. Federal Reserve data revealed that the durable goods manufacturing output index decreased in October by 1.3% after gaining 0.1% in the prior month. Durable goods output in October was 1.6% below year-ago levels.

Tubing-intensive sector performance was dominated by the autoworkers strike, which pushed the output of motor vehicles and parts down by 10.0%. Other tubing-intensive sectors were mixed as gains in electrical equipment, appliances, and components (+1.5%) and aerospace and other miscellaneous transportation equipment (+1.0%) helped to offset declines in fabricated metal products (-0.1%), machinery manufacturing (-0.7%), and furniture and related products (-1.4%).

Primary metals output, affecting the availability and cost of welded pipe and tube raw materials, decreased by 1.7% in October. The October Manufacturing Report On Business®, as published by the Institute for Supply Management® (ISM®), indicated continued weakness in the manufacturing sector that has endured for 12 consecutive months. The latest report noted that the Purchasing Managers’ Index (PMI®) fell 2.3 percentage points from the September level to 46.7. The October New Orders Index also dropped from the September survey by 3.7 points to 45.5. The Production Index reading of 50.4 was a 2.1-percentage point decrease compared to September’s figure of 52.5. The combination of a slightly positive production index and a falling new orders index led to a decrease in the backlog index reading for October to 42.2.

ISM Chair Timothy R. Fiore, CPSM, C.P.M., noted that the domestic manufacturing sector continued to contract at a faster rate in October.

“Seventy-five percent of manufacturing gross domestic product [GDP] contracted in October, up from 71% in September,” Fiore said. “More importantly, the share of sector GDP registering a composite PMI calculation at or below 45%—a good barometer of overall manufacturing weakness—was 37% in October, compared to 6% in September and 15% in August. Three of the top seven industries by contribution to manufacturing GDP fell into this category.”

Tubing-intensive industries reporting contraction in October, in the following order, were electrical equipment, appliances, and components; machinery; fabricated metal products; furniture and related products; and transportation equipment. For more information, visit www.ismrob.org.

About two months after announcing a temporary idling of blast furnace B at its Granite City, Ill., steel plant U.S. Steel has announced that the idling will be indefinite. Steel rolling and finishing operations will continue at the plant using slabs from other facilities. The company continues to evaluate offers received to buy all or part of it.

The UAW strike came to a close in early November as GM reached an agreement that was largely in line with deals that had been struck with Ford and Stellantis. Membership approved the new contract at all three companies by mid-November.

Preliminary overall pipe and tube shipments in October for the sectors of the market that we cover increased from September by about 10.4%, as imports increased by about 23% from a September low point and domestic shipments moved up by about 4%. These shipment numbers are subject to change as shipment data is finalized. Compared to a year ago, preliminary October shipments were lower by 6.2%, primarily on lower import volumes. Manufacturing and construction product shipments in October were flat as compared to a year ago but increased by 5.1% from September on a 17% gain in import volumes.

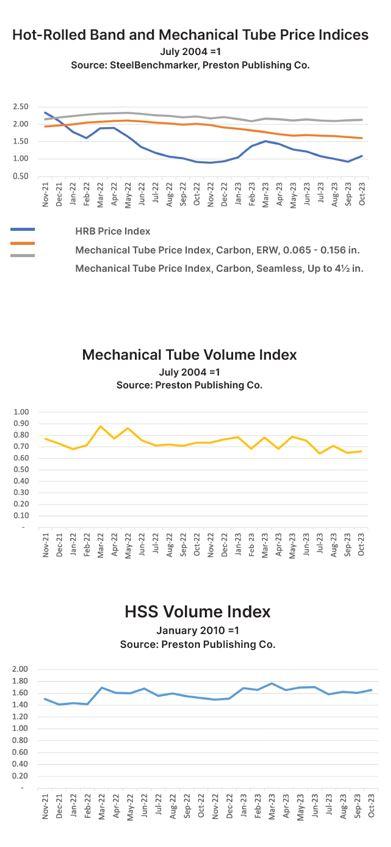

For mechanical tubing products, those most closely associated with manufacturing activity, October preliminary shipments were up by 2.0% from the September level but registered 10.0% below a year ago as manufacturing activity continued to decline.

The U.S. Federal Reserve has not raised interest rates since its July 26, 2023, meeting, and the U.S. economy continued to perform. Odds of a recession within the next year in the U.S. remain elevated but are decreasing. Consumer spending remains resilient despite a resumption of college loan repayments and rising credit balances. Job gains are slowing, as is inflation. Fuel prices are lower as of this writing, but OPEC+ just announced an additional million-barrel-per-day production cut.

According to data from the SteelBenchmarker, the index for base hot-rolled band prices moved up to 1.08 in October from 0.92 in September. Data suggests that prices have continued to increase on a series of increase announcements that started in mid-October led by Cleveland-Cliffs. The most recent announcement as of this writing was by Nucor on Nov. 27, which set its base price at $1,100/ton effective immediately with new orders.

The Tube and Pipe Journal became the first magazine dedicated to serving the metal tube and pipe industry in 1990. Today, it remains the only North American publication devoted to this industry, and it has become the most trusted source of information for tube and pipe professionals.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

In this episode of The Fabricator Podcast, Caleb Chamberlain, co-founder and CEO of OSH Cut, discusses his company’s...